Every project faces risks. Some risks are known, while others appear without warning. To handle both, project managers set aside two types of reserves: contingency reserve and management reserves. A contingency reserve covers known risks you can plan for, like price changes or minor delays. A management reserve addresses unknown risks that may arise during the project.

Knowing how to use these reserves keeps your project on track and your budget safe.

In this blog post, I will explain both reserves, their differences, give clear examples, and show how to plan your reserves.

What is a Contingency Reserve?

A contingency reserve is a budget or time allowance for risks you have identified in your risk register—in other words, “known unknowns.” The reserve is part of the cost baseline or schedule baseline.

“Contingency reserve is a budget set aside to manage identified risks.”

Types of Contingency Reserves

Contingency reserve can be of the following types:

- Cost contingency reserve (e.g., extra $ for material cost increase)

- Time contingency reserve (e.g., buffer days for delays)

- Resource contingency reserve (e.g., extra staff or equipment ready to deploy)

How to Calculate Contingency Reserve

You can follow the following technique to calculate the contingency reserve for your project:

Percentage of Project Cost

For quick setups in small to medium projects, apply 3-10% of the total budget. Base the figure on risk perception—higher for volatile industries like construction. This method saves time but lacks precision for high-stakes work.

Expected Monetary Value (EMV)

EMV quantifies risks statistically: multiply each risk’s Probability by its Impact, then sum.

Formula: EMV = Probability × Impact.

Consider four risks:

| Risk | Probability | Impact (USD) | EMV (USD) |

| A | 30% | 5,000 | 1,500 |

| B | 50% | 2,000 | 1,000 |

| C | 20% | 10,000 | 2,000 |

| D | 10% | 5,000 | 500 |

| Total | 5,000 |

This totals $5,000, but not all risks materialize. The pool spreads coverage: occurring risks draw funds, unrealized ones offset. For a few risks, supplement with other methods to avoid shortfalls.

EMV assumes independence, a common pitfall.

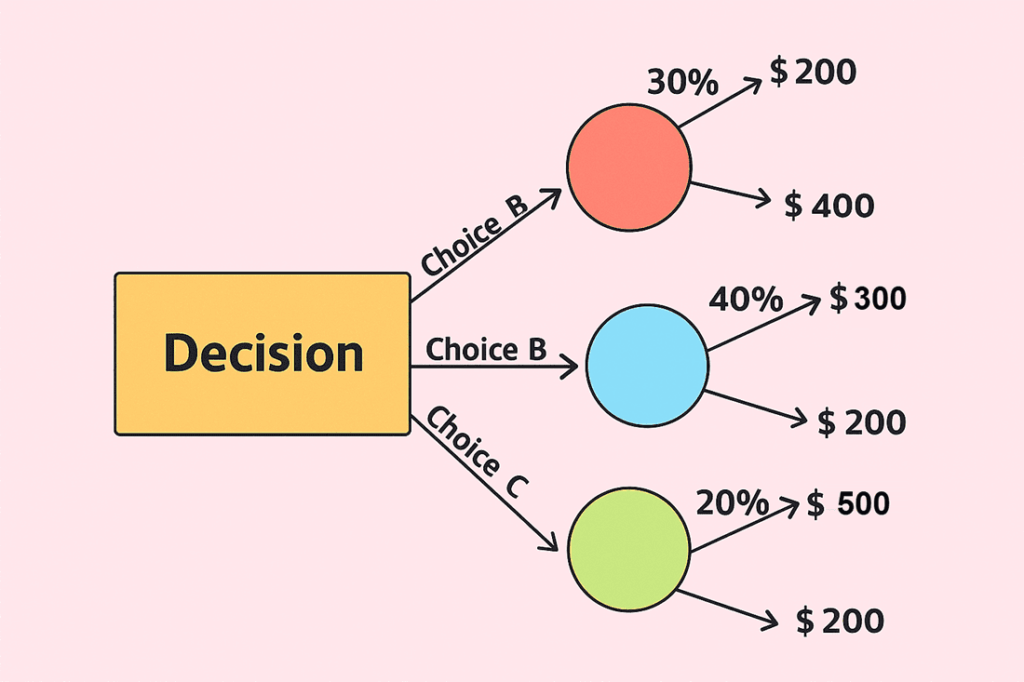

Decision Tree Analysis

Map decisions visually to pick optimal paths. Calculate EMV for branches, favoring the highest (for opportunities) or the lowest negative (for threats).

Example: Three vendor choices for a software rollout.

- Choice A: 30% chance of $200K profit, 70% of $400K ? EMV = (0.3 × 200) + (0.7 × 400) = $340K

- Choice B: 40% of $300K, 60% of $200K -> EMV = $240K

- Choice C: 20% of $500K, 80% of $200K -> EMV = $260K

Select A for max gain. This technique shines in multi-outcome scenarios.

Monte Carlo Simulation

Run thousands of iterations on variables like durations to predict outcomes. Using PERT estimates (optimistic, most likely, pessimistic), simulate schedules.

Example:

| Activity | Optimistic | Most Likely | Pessimistic | PERT Estimate |

| A | 4 | 5 | 8 | 5.3 |

| B | 5 | 6 | 7 | 6 |

| C | 6 | 7 | 8 | 7 |

| Total | 15 | 18 | 23 | 18.3 |

Based on the PERT estimate, these three activities are expected to finish in about 18.3 months. In the best case, they may end in 15 months, while in the worst case, they could take up to 23 months.

If we run a Monte Carlo simulation for these tasks 500 times, it will generate results showing maybe a 2% chance of completing the project in 16 months, a 70% chance in 19 months, and a 95% chance in 20 months.

You can also apply the Monte Carlo simulation to the project budget. For instance, adding 20,000 USD to the budget might give you a 70% chance of finishing within the budget. Increasing it by 40,000 USD could raise that Probability to 95%.

Clearly, this technique provides valuable insights that help you make more accurate and confident project decisions.

Why it matters:

Suppose you incorporate contingency reserves into your baseline. In that case, you are less likely to incur cost or schedule overruns when one of the identified risks materialises.

Recent research shows that using more advanced methods (e.g., Monte Carlo simulation) that account for various types of uncertainty yields more reliable reserve estimates.

What is Management Reserve?

A management reserve covers risks you did not identify—“unknown unknowns.” It sits outside the cost baseline (for cost reserve) or schedule baseline and is controlled at the management/sponsor level.

For example, a vendor unexpectedly collapses mid-project, requiring a major restructure. You call on the management reserve.

Key formulas:

- Cost Estimate: Sum of all work packages.

- Cost Baseline: Cost Estimate + Contingency Reserve.

- Project Budget: Cost Baseline + Management Reserve.

When to use Management Reserve

- When an entirely new risk emerges that was not in your risk register

- When changes in scope or external shocks (“black swan” events) hit your project

- Only after approval, because the project manager typically cannot use it on their own authority

When Not to Use Management Reserve

In the following case, dont use management reserve:

- Overruns: Re-estimate and approve a new baseline; don’t patch poor planning.

- Schedule Compression: Crashing or fast-tracking spawns new risks—update contingency first.

- Gold Plating: Avoid scope extras; they inflate risks.

- Fallback Plans: These backup known contingencies—use the other reserve.

- Residual Risks: Handled via contingency for identified leftovers.

Key points:

- It is not part of the cost baseline; it sits in the project budget above baseline.

- It often requires formal change-control or sponsor approval.

- Some organizations skip it; instead, the project manager must request extra funding when surprises arise.

Key Differences: Contingency vs Management Reserve

The following table shows the key difference between contingency reserve and management reserve:

| Feature | Contingency Reserve | Management Reserve |

| Risk type | Known risks (identified) | Unknown risks (not identified) |

| Inclusion in baseline | Yes – cost or schedule baseline | No – sits above baseline |

| Authority to access | Project manager (usually) | Senior management or sponsor |

| Timing of use | As soon as the identified risk occurs | When a new risk or change request arises |

| Example | Material cost increase identified in the risk register | Vendor collapse, regulatory law changes unexpectedly |

By remembering: “Contingency = known unknowns; Management = unknown unknowns,” you’ll keep the difference clear.

How to Estimate Reserves (With Real-World Data)

Contingency Reserve Estimation Methods:

- Percentage-Based: e.g., allocate 5–10% of total cost if risks are moderate.

- Expected Monetary Value (EMV): Sum of (probability × impact) per risk. See the example earlier.

- Monte Carlo Simulation: Map many scenarios of cost/schedule impact, compute confidence levels (e.g., 80% chance treatable with reserve). A recent paper shows this method accounts for both aleatoric and epistemic uncertainties.

Management Reserve Sizing:

- Often based on organisation policy or project complexity rather than a detailed risk register.

- For high-uncertainty projects (e.g., innovative, untested domains), the reserve may be larger.

- Some firms set it at 5-15% of the total budget (though this is more of a rule of thumb than a scientific finding).

Real-world tip for you (e.g., building a multi-story construction project):

- Suppose you are projecting a cost of USD 10 million and you identify six risks with EMV totalling USD 600,000. In that case, you may set your contingency reserve at USD 600k (or round up to USD 650k).

- Then consider industry uncertainty (weather, supply chain, regulation) and set a management reserve of USD 500k (5% rule) under management approval.

- Track usage; each time you draw from contingency, update the risk register and adjust the remaining reserve baseline.

Best Practices for Using Reserves in Your Projects

- Document Clearly: show how you derived the contingency reserve, what calculation or percentage was used. Transparency boosts trust.

- Communicate to Stakeholders: let sponsors see the reserve is not “extra padding” but a risk-management tool.

- Monitor and Track Use: once a risk is realised and the reserve used, update your baseline and reserve status.

- Release Unused Reserves: if risks do not occur, you can redeploy the budget or return it.

- Differentiate Usage: don’t misuse contingency for scope creep; similarly, don’t treat management reserve as automatic. Approval and control are key.

- Internal Link Suggestion: link to your other article “Schedule Reserve vs Contingency Reserve” (if you have one) — suitable for internal SEO.

- Visual Aid: Consider adding a simple infographic showing baseline, contingency, and management reserve layers. Provide alt-text like “Diagram showing cost baseline, contingency reserve, and management reserve layers.”

FAQ

Q1. Can a project manager use management reserve without approval?

No — management reserve typically requires sponsor or governance approval before use.

Q2. Does contingency reserve appear in the cost baseline?

Yes — contingency reserve is part of the cost baseline for known risks.

Q3. Which reserve covers unknown unknowns?

Management reserve covers risks that weren’t identified in the risk register.

Q4. If a risk is identified but no response is planned, which reserve applies?

That is a grey area. Generally, contingency reserve should cover identified risks with response plans; unaddressed risks may push you toward management reserve if they materialise.

Q5. Why might a project have no management reserve?

Some organizations rely on ad hoc approval for additional funding rather than pre-allocating a management reserve. This may reduce upfront budget, but increases the risk of funding delays.

Summary

Understanding the difference between contingency and management reserves helps you manage risks more effectively. Contingency reserves handle known risks, while management reserves cover the unexpected. Together, they protect your project’s cost, schedule, and success.

Always document how you set these reserves and review them regularly as your project progresses. Clear planning, communication, and control ensure you use reserves wisely. With this approach, you’ll stay prepared for both expected and surprise challenges in any project.

Further Reading:

- What is a Contingency Plan?

- What is Contingency Reserve in Project Management?

- What is the Fallback Plan?

- Contingency Plan Vs Fallback Plan

- Mitigation Vs Contingency Plan – Key Differences and How to Use Both

- What is Management Reserve in Project Management?

This topic is important from a PMP and PMI-RMP exam point of view. You may see a few questions on this topic in your exam.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.

Hi Fahad

I am not sure if the EMV of all identified risk will be part of the contingency reserve. The Contingency reserve is associated with the Active Acceptance of the risk. The Project Manager prepares a contingent plan with pre-set triggers and contingency budget is set to execute this plan. However, the cost to mitigate any threat should be part of the project cost and not of the contingency reserve. Will you please give reference to the PMBOK which states that EMV of all identified risk without a risk mitigation should be part of the contingent reserve?

You may not create a contingency reserve for risks who are in watch list or you decide to passively accept them.

Fahad –

I am having trouble deciphering the following from PMP book. Any help would be appreciated.

1. On Pg. 173, it states that activity cost estimates may include contingency reserves…and then says contingency reserves are part of funding requirements. Then on Pg. 177 it mentions that reserves are not included in the project cost baseline but can be included in the total project budge? Leaving aside the issue of management reserves, are contingency reserves included in cost baseline or not? How do we reconcile these two different conflicting passages in PMBOK 4?

2. Are contingency reserves layered? In other words, do we have contingency reserves at the activity level and then also contingency reserves at the work package / control account level?

3. (optional question if you can answer): If time spent on the project = cost incurred, then we have activity duration estimation reserves as well as activity cost reserves (both of these amount to additional cost from pure economic perspective)? Isn’t this double dipping or both of these reserves are reconciled at some point in the project?

4. Lastly, in the practical world, do project managers maintain 2 different cost buckets for each work package: original cost & contingency reserve or both of them are merged into one cost number for a package?

Thanks

1. On page-173, the PMBOK is talking about the contingency reserve that cost estimate may include the contingency reserve. On page-177, the PMBOK Guide is talking about the management reserve that it is not included in the cost baseline but in the total budget. Contingency reserve is included in the cost baseline while management reserve is not.

budget = cost baseline + management reserve

2. Contingency reserve is a pool of amount which is utilized when any identified risk occurs. Contingency reserve is calculated for whole project considering positive risk and negative risks.

3. The way you have calculated the contingency reserve for cost, you also have to calculate the contingency reserve for schedule, here they are called time reserve of buffers. Please see page-151 PMBOK 4th edition.

4. Answer for this point is melted in above explanation.

Hope it helps.

Hello Fahad,

I have a question on CR. CR, as we all know, are the reserves used to cover the costs of known-unknowns. It is said that CR is calculated using EVM, which is a part of Perform Quantitative Analysis process of Risk Management. Now, we also know that this process is optional – if the cost of doing Perform Quantitative Analysis is high, it can be skipped altogether. Does it mean that calculating CR without doing a quantitative analysis a guesswork?

Sumeet

The process for establishing Contingency Reserve is established in the Risk Management Plan. It can be set using EMV, but that’s not required. Some organizations set the contingency as a fixed rate (e.g. 10%). Others set it using a risk model (generally a high-level questionnaire to determine the relative level of risk compared to other projects). And yes, some set it using expected value.

The key is to know which process you’re going to apply. If you are ONLY going to use EMV, then you need to set down Quantitative Analysis as a process step that shall not be skipped. If you’re going to use some other metric to set it, you’re free to include or exclude the Quantitative Analysis.

Hope it helps.

Thanks Fahad, this certainly helps!

Hi Fahad,

I’m new to this area of project management, so apologies if this seems like a silly question! Since the Contingency Reserve is calculated as a percentage of the impact of the risk occurring, the reserves are never actually going to cover the impact if the risk does actually occur, correct?

So if the risk does occur, the effort to resolve the risk means your contingency will be used AND you will also have a deviation from your cost baseline? While I appreciate that you can’t factor in the complete cost of every risk, I’m having difficulty in seeing the logic of this method of estimating contingency reserves when it seems like they will never completely cover the cost of ANY risk?

Is it possibly the assumption that, if the risk was to occur, that the contingency plan for a risk factors in additional activities to reduce the cost of the impact, meaning that when combined with the contingency plan, the contingency reserves do actually cover the cost of the risk?

Kind Regards,

Eoin

Hello Eoin,

First of all you should understand that risk can be managed as an aggregate for the large population of events (macro), or it can be managed on an event-by-event (micro) basis.

In project management, Risk Management is managed by considering a large population of events.

Now, come to your point:

Let’s say that you have identified a hundred numbers of risks and then calculated the impact of these risks if they happen to occur. Then you multiply the impact by their respective likelihood and add them all to get the contingency reserve.

Now, do you really think that these all hundred identified risks are going to occur on your project? No, there is very less chance for this to happen.

Point is, some of them will occur and rest will not occur. In case of any risk occurs, you take money from the contingency reserve.

There will not be any deviation from the cost baseline unless you spend all of your contingency reserve.

Hi Fahad,

Thanks for the reply on this, what got me about the examples I saw on this section is that there was never enough contingency to cover if even a single risk occurred.

Take a simple scenario where you have identified 6 risks, all with a €10,000 impact and 10% chance of occurrence, if just one of these risks occurred, all your contingency is used up and you still have not covered the cost of the risk!

I take the point that in a larger project the number of risks is much larger, therefore your contingency reserve will be more likely to cover the cost of risks occurring, perhaps the examples involving smaller numbers of risks are just not realistic?

Hello Eoin,

As I said earlier that Project Risk Management is managed by considering a large population of events.

As the population grows, better the Risk Management Plan.

Hope it helps.

Fahad

If the allocated cost of a contingency plan for a single risk event exceeds the total remaining funds in a contingency reserve, where the contingency reserve is managed in aggregate (sum of probability x impact for all accepted risks with contingency plans), then I think there would be a strong case to treat this as an unknown-known. I generally consider these planning errors, but in this case, the planner is not necessarily at fault, since allocating funds for the contingency reserve must be balanced against the statistically expected cost for the risks in order to keep an acceptable cost baseline.

I would suggest that the minimum amount for the contingency reserve should always be enough to cover the largest remaining risk in the contingency plan. So in your example, instead of establishing a €6,000 contingency reserve (6 x €10,000 x 10%), impose a constraint that the contingency reserve is never less than €10,000 until that last trigger event is safely in the rearview mirror.

It is your project and you have to manage it. The PMBOK Guides equip you with the best industry knowledge so that you can complete the project successfully.

Develop the project plan as per your knowledge and understanding, get it approved and stick to it.

First of all thanks for a nice post. My doubt is:

Assuming there is a contingency plan exisitng for an identified risk, and subsequently the risk does occur, in this case my schedule will be changed taking into account the contingency. So do we have to perform integrated change control, take it to the advisory board, get an approval and then change the baselines? – because there is an identified risk

occurence..

In this case are we using management reserves or contingency reserves? If it’s contingency reserves then what is the use of it when my baselines are still changing?

Thanks in advance.

Hello Anmol,

If any identified risk occurs, you implement the approved contingency plan. In this case you will not go for schedule change because risk was already identified and it was already factored in your schedule.

For identified risks, Contingency Reserve is used. Management Reserve is for unidentified risks.

There is no change in the baseline unless you spend all contingency reserve.

Nice post, but if i have risks and probabilities of their occurance, how can i calculate both Contingency and management reserve ?!

Hello Nora,

To calculate Contingency Reserve, you must have probability of each risk and its impact. Once you get it, multiply probability to its impact. Repeat this procedure for all risks and then add it. Result will be your contingency reserve.

Management reserve is a some percentage of the cost of the project. It may vary between 5 to 10%.

I have one Question regarding Secondary Risk , is it covered by Contingency Or Management reserve ?

Thank you

Since it is a known or identified risk, it is covered under contingency reserve.

I have undersrtood the following:

1. Neither the CR or the MR are included in the cost baseline.

2. The CR is included in the project's budget (i.e., required funding)

3. The MR is not incliuded in the project's budget (i.e., required funding)The exposure draft of the 5th Edition of the PMBOK Guide espouses the following

1. The CR is included in the cost baselne

2. The MR is not included in the cost baseline, but is included in project's budget (i.e., required funding)

What are your thoughts?

As per the PMBOK Guide 4th Edition,

Cost base line is the sum of project cost estimate and contingency reserve; i.e.

Cost Baseline = Project Cost Estimate + Contingency Reserve

And, project budget is the sum of project cost base line and the management reserve; i.e.

Project Budget = Cost Baseline + Management Reserve

Therefore, Management Reserve is not a part of the cost baseline but it is a part of the project budget and Contingency Reserve is a part of cost baseline as well as project budget.

Hope it answers your query.

Since, I’ve not reviewed the exposure draft of the PMBOK Guide 5th edition thoroughly, I would not comment on it. However, the information provided by you here in comment section is agreeing with the current version of the PMBOK Guide; i.e. 4th edition.

An additional follow-up question:

If a negative risk (theat) is actively accepted, good practice would require that we develop a contingent plan of action (response) that woulf be executed should thwe risk be realized. The implementation of that response would require that we use established formal change control procedures to modify the scope, schedule and/or cost baselines as necessary. If a modification of the cost baseline is needed.and we have estiblished both a Contingency Reserve and a Management Reserve of money, where would the funds to cover the contingent response come from?

If any identified risk occurs then fund from the Contingency Reserves will be used, otherwise Management Reserved will be used but only after taking the required approval from the management.

It is a fact that the cost baseline is the sum of the cost estimates of each work package. Every dollar of the cost baseline must be linked to a component of the projects scope. If, as you replied earlier, the Contingency Reserve (CR) funds are included in the baseline, what element of scope are they tied to before possibly being moved to funding a contingent response for an actively accepted risk?.

The PMBOK Guide 4th Edition, Page 173, Article 7.1.2.6 says,

"Cost estimates may include contingency reserves (sometimes called contingency allowances) to

account for cost uncertainty."

This is a separate reserve, known as a CR and this reserve is not tied with anything. Just a calculated reserve for identified risks.

Scott Freauf says

June 25, 2012 at 9:08 PM

I have undersrtood the following:

1. Neither the CR or the MR are included in the cost baseline.

2. The CR is included in the project’s budget (i.e., required funding)

3. The MR is not incliuded in the project’s budget (i.e., required funding)The exposure draft of the 5th Edition of the PMBOK Guide espouses the following

1. The CR is included in the cost baselne

2. The MR is not included in the cost baseline, but is included in project’s budget (i.e., required funding)

What are your thoughts?

Does 3 not contradict the second 2. The MR is not included in the cost baseline, but is included in project’s budget (i.e., required funding)

What are your thoughts?

Please refer to page 213, PMBOK Guide fifth edition and the diagram. It will clear your all doubt regarding the CR, MR, cost baseline, and project budget.