Risks occur in every project, and as a project manager, it is your responsibility to manage them as they occur. These risks can be identified or unidentified. If these risks are identified, you will implement the contingency plan; otherwise, you will manage them through a workaround.

You will use the contingency reserve and management reserve to manage these risks. These reserves are defined during the risk management planning process. The contingency reserve and management reserve provides you with a cushion against the risks and are part of your project budget.

Many professionals assume these reserves are the same since they serve the same purpose. Generally, small and medium-sized organizations do not differentiate between them and take them as a percentage of the project cost to keep things simple. Therefore, professionals with experience with these organizations may not know the difference between contingency and management reserves.

Contingency Reserve

You manage identified risks with the contingency reserve. This reserve can be in either cost or time.

The contingency reserve is not random; it is an estimated reserve based on various risk management techniques.

Project managers control this reserve; they have full authority to use it whenever an identified risk occurs. They can also delegate this authority to a risk owner. The risk owner will manage it and update the project manager later.

How to Calculate the Contingency Reserve

There are various techniques to calculate the contingency reserve. Some of them are as follows:

- Percentage of the Project’s Cost

- Expected Monetary Value

- Decision Tree Analysis

- Monte Carlo Simulation

Now, we will discuss each technique in detail.

Percentage of the Project’s Cost

Small and medium-sized organizations use this technique for small projects; it helps save money and resources.

You take a percentage of the cost of the project to calculate the contingency reserve, which usually lies between 3% and 10%. This number is based mainly on the perceived risk of the project.

Expected Monetary Value

Expected monetary value is a statistical technique used to quantify risks and help calculate the contingency reserve. This technique is used in medium to high-cost projects where the stakes are too high to risk the project failing.

To find the expected monetary value, first, you will calculate the probability and impact of each event, then multiply them together to generate the EMV of each risk.

Expected Monetary Value (EMV) = Probability * Impact

Then, add the calculated EMV of all identified risks together.

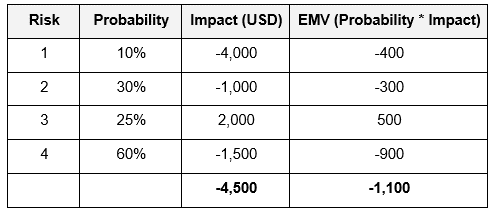

Example

Assuming you have four risks with probabilities and impact:

From the above table, you could argue that the funds needed to manage all identified risks is 4,500 USD, but this would be incorrect.

Not all possible risks are guaranteed; some may happen, and some may not. All risks will add their EMV to the pool. The risks that do occur will use money from the pool, but the risks that do not occur will help cover the cost of those that did.

In the above scenario, you may need to add 1,100 USD to your budget to cover all identified risks.

The expected monetary value concept works well when you have many risks because the more you can identify, the better the spread of the reserve. If you have identified fewer risks, there will not be enough spread, and the reserve may dry up.

The EMV technique has a few drawbacks, which include:

- You assume that all risks are independent, which is not always the case.

- If the number of risks is small, the spread will be less, and the reserve may be insufficient.

- There is a chance of avoiding positive risks, which may lead to a false result.

Decision Tree Analysis

Decision tree analysis is a quantitative risk analysis technique. This technique helps you select the best choice. This graphical technique looks like a tree, hence its name.

Here, you determine the expected monetary value of each event and select the best choice.

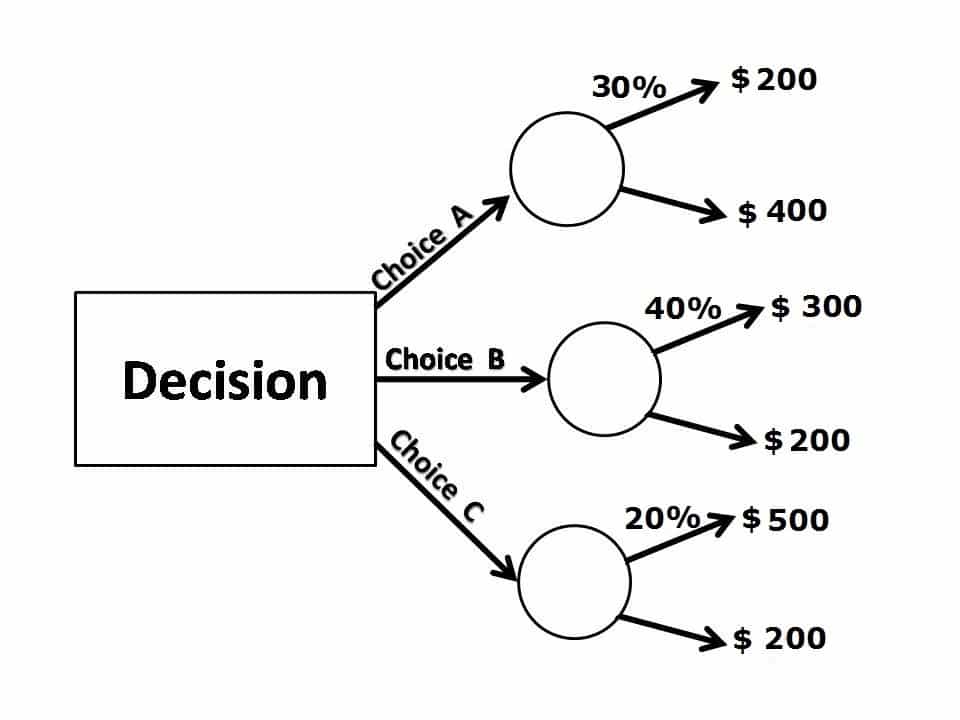

Example:

Calculate the expected monetary value of the best choice.

In this example, you have three choices: Choice A, Choice B, and Choice C.

As seen from the figure above, all three choices represent opportunities. Therefore, you will find the expected monetary value of the three events and go with the most favorable. You are trying to get the maximum profit.

Now, let us calculate the EMV of all three events.

In the diagram, you were given the probability of one event, while the probability of the other event is not provided. To find the other probability, you have to subtract the probability of the first event from 100, because the sum of all possible outcomes for one event is 100%.

EMV of Choice A = 0.30*200 + 0.70*400

= 60 + 280

= 340 USD

EMV of Choice B = 0.40*300 + 0.60*200

= 120 + 120

= 240 USD

EMV of Choice C = 0.2*500 + 0.80*200

= 100 + 160

= 260 USD

You have to choose the one with the highest EMV, which is Choice A.

Note that you select the least negative option if all risks are negative. This is because you want to spend the least money on managing risks.

Monte Carlo Simulation

In 1940, an atomic nuclear scientist named Stanislaw Ulam invented this technique and named it Monte Carlo after the city in Monaco, which is famous for its casinos.

This technique gives several possibilities of outcomes and the probabilities for any choice of action.

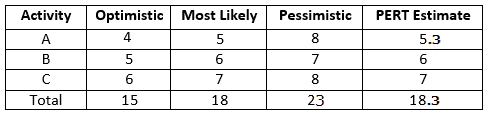

For example, we will discuss using the Monte Carlo simulation in analyzing a project schedule. To use this technique, you must have duration estimates for each activity.

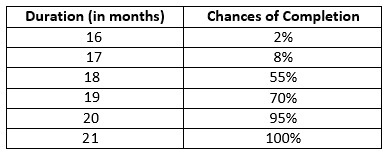

You have three activities with the following estimates (in months):

According to the PERT estimate, these three activities will end in 18.3 months.

In the best case, it will take 15 months, and in the worst case, it may take 23 months.

Now, if we run the Monte Carlo simulation for these tasks, five hundred times, it will show us results like this:

(The above information is only for illustration purposes and is not from an actual Monte Carlo simulation test result.)

After reviewing the results, you can determine that there is a 2% chance of completing the project in 16 months, or a 70% chance of completing the project in 19 months, or a 95% chance of completing the project in 20 months, etc.

Likewise, you can run the Monte Carlo simulation for the budget.

For example, you can generate data like adding 20,000 USD to the project cost, giving you a 70% chance of completing the project within the budget. If you add 40,000 USD to the project cost, there is a 95% chance that you can complete the project within the budget, etc.

So, it’s clear that with the use of this technique, you can get valuable information that will help you make better-informed decisions.

As you proceed, you will become more familiar with the situation, and you can review this contingency reserve again. This reserve can be reduced if required, and you can release the funds.

Management Reserve

The management reserve is the cost or time reserve used to manage the unidentified risks or “unknown-unknown.”

The management reserve is a part of the project budget but not the cost baseline. It is not an estimated reserve; it is a figure that is fashioned according to the organization’s policies.

It can be 5% of the total project cost or duration of the project, or it may be as high as 10%. The management reserve is usually estimated based on the uncertainty of the project.

For example, if you are doing a project in which your organization has the expertise and experience, the management reserve will be less. In this case, there is less uncertainty.

However, if you are doing a new kind of project for your organization, the management reserve will be high because, in this situation, the uncertainty is greater.

The project manager does not control the management reserve; the management does. Therefore, the project manager must receive approval to use this reserve whenever any unidentified risk occurs.

Many organizations try to avoid using the management reserve. They think if the project manager has to come to them every time to get approval, why keep it separate? The project manager can come whenever they need extra money, so why have a management reserve?

On the PMP exam, you will see many questions on contingency reserve, management reserve, cost estimate, and the project budget. These are crucial concepts; without these reserves, you cannot estimate the cost baseline and project budget. Therefore, for your easy reference, I am explaining these topics here as well.

Cost Estimate

The cost estimate is the cost of all work packages and is “rolled up” to the top level; this is the total cost of the project.

Cost Baseline

You get the cost baseline when you add the contingency reserve to the cost estimate.

Cost Baseline = Cost Estimate + Contingency Reserve

Note that the project’s performance will be measured against the cost baseline.

Project Budget

You will get the project budget if you add the management reserve to the cost baseline.

Project Budget = Cost Baseline + Management Reserve

When You Cannot Use the Management Reserve

Management reserve and contingency reserve are different and serve different purposes.

Below are a few cases where you should not use the management reserve.

When You Are Over Budget

You have to estimate the new budget and try to get it approved. You should never use the management reserve to compensate for cost overrun.

The management reserve is for unidentified risks, not to cover the cost overrun.

While Using Schedule Compression Techniques

There are two schedule compression techniques: fast-tracking and crashing.

Schedule compression may lead to new risks. Identify those risks, prepare a response plan, and calculate the new contingency reserve. You will need to get it approved.

You can revisit your management reserve for a review as well.

However, in crashing, you use extra resources. After you complete the planning for crashing, you have to revisit your risk management planning.

Gold Plating

You should avoid gold plating, and you should not use the management reserve for it; this increases the risk and changes the scope.

Fallback Plan

I often receive emails from visitors asking me why we cannot use the management reserve for the fallback plan.

By definition, the management reserve is used for unknown risks.

A fallback plan is not used for unknown risks; it is a plan for known risks when the primary response plan fails. Therefore, you will use the contingency reserve for this plan, not the management reserve.

Residual Risks

Since residual risks are identified risks, you will use contingency reserve to manage these risks.

The Difference Between Contingency Reserve and Management Reserve

The following are a few differences between the contingency reserve and management reserve:

- The contingency reserve manages identified risks, while the management reserve is used for unidentified risks.

- The contingency reserve is an estimated figure, while the management reserve is a percentage of the cost or duration of the project.

- The project manager has authority over the contingency reserve, while the management reserve needs the management’s permission.

- The contingency reserve is a part of the performance measurement baseline, while the management reserve is not.

Summary

To complete your project successfully, you must be proactive in risk management. The contingency reserve and management reserve are the backbones of your risk management, as they provide the means to manage risks. The contingency reserve and management reserve are not the same; they are calculated with different techniques and serve different purposes. The contingency reserve is for identified risks and part of your cost baseline, while the management reserve is for unidentified risks and is a part of your budget.

This topic is important from a PMP and PMI-RMP exam point of view. You may see a few questions on this topic in your exam.

How do you calculate the management reserve and contingency reserve on your projects? Please share your thoughts in the comments section.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.

Hi Fahad

I am not sure if the EMV of all identified risk will be part of the contingency reserve. The Contingency reserve is associated with the Active Acceptance of the risk. The Project Manager prepares a contingent plan with pre-set triggers and contingency budget is set to execute this plan. However, the cost to mitigate any threat should be part of the project cost and not of the contingency reserve. Will you please give reference to the PMBOK which states that EMV of all identified risk without a risk mitigation should be part of the contingent reserve?

You may not create a contingency reserve for risks who are in watch list or you decide to passively accept them.

Fahad –

I am having trouble deciphering the following from PMP book. Any help would be appreciated.

1. On Pg. 173, it states that activity cost estimates may include contingency reserves…and then says contingency reserves are part of funding requirements. Then on Pg. 177 it mentions that reserves are not included in the project cost baseline but can be included in the total project budge? Leaving aside the issue of management reserves, are contingency reserves included in cost baseline or not? How do we reconcile these two different conflicting passages in PMBOK 4?

2. Are contingency reserves layered? In other words, do we have contingency reserves at the activity level and then also contingency reserves at the work package / control account level?

3. (optional question if you can answer): If time spent on the project = cost incurred, then we have activity duration estimation reserves as well as activity cost reserves (both of these amount to additional cost from pure economic perspective)? Isn’t this double dipping or both of these reserves are reconciled at some point in the project?

4. Lastly, in the practical world, do project managers maintain 2 different cost buckets for each work package: original cost & contingency reserve or both of them are merged into one cost number for a package?

Thanks

1. On page-173, the PMBOK is talking about the contingency reserve that cost estimate may include the contingency reserve. On page-177, the PMBOK Guide is talking about the management reserve that it is not included in the cost baseline but in the total budget. Contingency reserve is included in the cost baseline while management reserve is not.

budget = cost baseline + management reserve

2. Contingency reserve is a pool of amount which is utilized when any identified risk occurs. Contingency reserve is calculated for whole project considering positive risk and negative risks.

3. The way you have calculated the contingency reserve for cost, you also have to calculate the contingency reserve for schedule, here they are called time reserve of buffers. Please see page-151 PMBOK 4th edition.

4. Answer for this point is melted in above explanation.

Hope it helps.

Hello Fahad,

I have a question on CR. CR, as we all know, are the reserves used to cover the costs of known-unknowns. It is said that CR is calculated using EVM, which is a part of Perform Quantitative Analysis process of Risk Management. Now, we also know that this process is optional – if the cost of doing Perform Quantitative Analysis is high, it can be skipped altogether. Does it mean that calculating CR without doing a quantitative analysis a guesswork?

Sumeet

The process for establishing Contingency Reserve is established in the Risk Management Plan. It can be set using EMV, but that’s not required. Some organizations set the contingency as a fixed rate (e.g. 10%). Others set it using a risk model (generally a high-level questionnaire to determine the relative level of risk compared to other projects). And yes, some set it using expected value.

The key is to know which process you’re going to apply. If you are ONLY going to use EMV, then you need to set down Quantitative Analysis as a process step that shall not be skipped. If you’re going to use some other metric to set it, you’re free to include or exclude the Quantitative Analysis.

Hope it helps.

Thanks Fahad, this certainly helps!

Hi Fahad,

I’m new to this area of project management, so apologies if this seems like a silly question! Since the Contingency Reserve is calculated as a percentage of the impact of the risk occurring, the reserves are never actually going to cover the impact if the risk does actually occur, correct?

So if the risk does occur, the effort to resolve the risk means your contingency will be used AND you will also have a deviation from your cost baseline? While I appreciate that you can’t factor in the complete cost of every risk, I’m having difficulty in seeing the logic of this method of estimating contingency reserves when it seems like they will never completely cover the cost of ANY risk?

Is it possibly the assumption that, if the risk was to occur, that the contingency plan for a risk factors in additional activities to reduce the cost of the impact, meaning that when combined with the contingency plan, the contingency reserves do actually cover the cost of the risk?

Kind Regards,

Eoin

Hello Eoin,

First of all you should understand that risk can be managed as an aggregate for the large population of events (macro), or it can be managed on an event-by-event (micro) basis.

In project management, Risk Management is managed by considering a large population of events.

Now, come to your point:

Let’s say that you have identified a hundred numbers of risks and then calculated the impact of these risks if they happen to occur. Then you multiply the impact by their respective likelihood and add them all to get the contingency reserve.

Now, do you really think that these all hundred identified risks are going to occur on your project? No, there is very less chance for this to happen.

Point is, some of them will occur and rest will not occur. In case of any risk occurs, you take money from the contingency reserve.

There will not be any deviation from the cost baseline unless you spend all of your contingency reserve.

Hi Fahad,

Thanks for the reply on this, what got me about the examples I saw on this section is that there was never enough contingency to cover if even a single risk occurred.

Take a simple scenario where you have identified 6 risks, all with a €10,000 impact and 10% chance of occurrence, if just one of these risks occurred, all your contingency is used up and you still have not covered the cost of the risk!

I take the point that in a larger project the number of risks is much larger, therefore your contingency reserve will be more likely to cover the cost of risks occurring, perhaps the examples involving smaller numbers of risks are just not realistic?

Hello Eoin,

As I said earlier that Project Risk Management is managed by considering a large population of events.

As the population grows, better the Risk Management Plan.

Hope it helps.

Fahad

If the allocated cost of a contingency plan for a single risk event exceeds the total remaining funds in a contingency reserve, where the contingency reserve is managed in aggregate (sum of probability x impact for all accepted risks with contingency plans), then I think there would be a strong case to treat this as an unknown-known. I generally consider these planning errors, but in this case, the planner is not necessarily at fault, since allocating funds for the contingency reserve must be balanced against the statistically expected cost for the risks in order to keep an acceptable cost baseline.

I would suggest that the minimum amount for the contingency reserve should always be enough to cover the largest remaining risk in the contingency plan. So in your example, instead of establishing a €6,000 contingency reserve (6 x €10,000 x 10%), impose a constraint that the contingency reserve is never less than €10,000 until that last trigger event is safely in the rearview mirror.

It is your project and you have to manage it. The PMBOK Guides equip you with the best industry knowledge so that you can complete the project successfully.

Develop the project plan as per your knowledge and understanding, get it approved and stick to it.

First of all thanks for a nice post. My doubt is:

Assuming there is a contingency plan exisitng for an identified risk, and subsequently the risk does occur, in this case my schedule will be changed taking into account the contingency. So do we have to perform integrated change control, take it to the advisory board, get an approval and then change the baselines? – because there is an identified risk

occurence..

In this case are we using management reserves or contingency reserves? If it’s contingency reserves then what is the use of it when my baselines are still changing?

Thanks in advance.

Hello Anmol,

If any identified risk occurs, you implement the approved contingency plan. In this case you will not go for schedule change because risk was already identified and it was already factored in your schedule.

For identified risks, Contingency Reserve is used. Management Reserve is for unidentified risks.

There is no change in the baseline unless you spend all contingency reserve.

Nice post, but if i have risks and probabilities of their occurance, how can i calculate both Contingency and management reserve ?!

Hello Nora,

To calculate Contingency Reserve, you must have probability of each risk and its impact. Once you get it, multiply probability to its impact. Repeat this procedure for all risks and then add it. Result will be your contingency reserve.

Management reserve is a some percentage of the cost of the project. It may vary between 5 to 10%.

I have one Question regarding Secondary Risk , is it covered by Contingency Or Management reserve ?

Thank you

Since it is a known or identified risk, it is covered under contingency reserve.

I have undersrtood the following:

1. Neither the CR or the MR are included in the cost baseline.

2. The CR is included in the project's budget (i.e., required funding)

3. The MR is not incliuded in the project's budget (i.e., required funding)The exposure draft of the 5th Edition of the PMBOK Guide espouses the following

1. The CR is included in the cost baselne

2. The MR is not included in the cost baseline, but is included in project's budget (i.e., required funding)

What are your thoughts?

As per the PMBOK Guide 4th Edition,

Cost base line is the sum of project cost estimate and contingency reserve; i.e.

Cost Baseline = Project Cost Estimate + Contingency Reserve

And, project budget is the sum of project cost base line and the management reserve; i.e.

Project Budget = Cost Baseline + Management Reserve

Therefore, Management Reserve is not a part of the cost baseline but it is a part of the project budget and Contingency Reserve is a part of cost baseline as well as project budget.

Hope it answers your query.

Since, I’ve not reviewed the exposure draft of the PMBOK Guide 5th edition thoroughly, I would not comment on it. However, the information provided by you here in comment section is agreeing with the current version of the PMBOK Guide; i.e. 4th edition.

An additional follow-up question:

If a negative risk (theat) is actively accepted, good practice would require that we develop a contingent plan of action (response) that woulf be executed should thwe risk be realized. The implementation of that response would require that we use established formal change control procedures to modify the scope, schedule and/or cost baselines as necessary. If a modification of the cost baseline is needed.and we have estiblished both a Contingency Reserve and a Management Reserve of money, where would the funds to cover the contingent response come from?

If any identified risk occurs then fund from the Contingency Reserves will be used, otherwise Management Reserved will be used but only after taking the required approval from the management.

It is a fact that the cost baseline is the sum of the cost estimates of each work package. Every dollar of the cost baseline must be linked to a component of the projects scope. If, as you replied earlier, the Contingency Reserve (CR) funds are included in the baseline, what element of scope are they tied to before possibly being moved to funding a contingent response for an actively accepted risk?.

The PMBOK Guide 4th Edition, Page 173, Article 7.1.2.6 says,

"Cost estimates may include contingency reserves (sometimes called contingency allowances) to

account for cost uncertainty."

This is a separate reserve, known as a CR and this reserve is not tied with anything. Just a calculated reserve for identified risks.

Scott Freauf says

June 25, 2012 at 9:08 PM

I have undersrtood the following:

1. Neither the CR or the MR are included in the cost baseline.

2. The CR is included in the project’s budget (i.e., required funding)

3. The MR is not incliuded in the project’s budget (i.e., required funding)The exposure draft of the 5th Edition of the PMBOK Guide espouses the following

1. The CR is included in the cost baselne

2. The MR is not included in the cost baseline, but is included in project’s budget (i.e., required funding)

What are your thoughts?

Does 3 not contradict the second 2. The MR is not included in the cost baseline, but is included in project’s budget (i.e., required funding)

What are your thoughts?

Please refer to page 213, PMBOK Guide fifth edition and the diagram. It will clear your all doubt regarding the CR, MR, cost baseline, and project budget.