Project managers often struggle to link day-to-day tasks with the big picture. How can you be sure your next project helps your company’s strategy? The Balanced Scorecard answers this question. Created by Robert Kaplan and David Norton, it is a strategic management tool that connects vision with action.

Unlike old performance systems that focused solely on financial metrics, the Balanced Scorecard considers four areas: financial, customer, internal process, and learning. When you apply this framework to projects, you align activities, track progress, and engage stakeholders.

This blog post explains the Balanced Scorecard, its benefits and drawbacks, its relevance to project management, and what the future holds.

Understanding the Balanced Scorecard

The Balanced Scorecard (BSC) is a strategic management framework that helps organizations turn their vision into clear actions and measurable results. Instead of focusing solely on financial outcomes, it considers performance from four interconnected perspectives: Financial, Customer, Internal Processes, and Learning and Growth.

In project management, the BSC ensures that projects do more than meet scope, time, and cost goals. It helps you align project objectives with business strategy, customer needs, efficient processes, and team capability development. By tracking balanced measures across these four areas, you can see how short-term project decisions affect long-term success.

The Balanced Scorecard provides a structured way to plan, monitor, and improve projects while keeping them aligned with organizational goals and sustainable growth.

The Four Perspectives in Balanced Scorecard

At the heart of the Balanced Scorecard are four perspectives that provide a holistic view of performance:

| Perspective | Focus |

| Financial | How well the organization uses resources and generates returns |

| Customer | How customers perceive the organization and how well it meets market needs |

| Internal Processes | How internal operations and processes support strategy |

| Learning & Growth | How the organization develops people, information systems, and culture to support long-term goals |

These perspectives encourage managers to balance today’s demands with tomorrow’s growth.

Financial perspective

The financial perspective focuses on economic health. For-profit organizations include revenue, profit margin, and return on investment. In nonprofit and public organizations, it may track cost efficiency or fundraising performance. Projects aligned with this perspective ensure that budgets, cost-benefit analyses, and risk management contribute to financial goals.

Customer perspective

This dimension looks at satisfaction, market share, brand recognition, and service quality. Questions such as “How do our customers see us?” guide targets and measures. Projects can help by improving stakeholder engagement, delivering features that meet client needs, and enhancing market positioning.

Internal processes perspective

Here, organizations ask, “What must we excel at?” Objectives focus on process improvements, quality optimization, resource utilization, and innovation. Projects contribute by streamlining workflows, improving quality management, and effectively leveraging organizational assets.

Learning and growth perspective

The last perspective, sometimes called organizational capacity, captures intangible drivers of success. It covers human resources (skills, training, culture), information capital (data systems, networks), and organizational culture. Investing in employee development and knowledge sharing ensures the organization can innovate and adapt.

Strengths and Weaknesses of the Balanced Scorecard

Strengths

The Balanced Scorecard aligns all areas of an organization with its strategy. It turns abstract visions into concrete actions and measures. Balancing financial and non-financial objectives, it encourages long-term thinking. It promotes transparency and improves communication—everyone knows how their work supports strategic goals.

In project environments, it provides a logical structure for selecting initiatives, setting KPIs, and controlling progress. Modern trends, such as integrating environmental, social, and governance (ESG) metrics into scorecards, allow firms to meet the expectations of conscious consumers and investors.

Weaknesses

The Balanced Scorecard is not a one-size-fits-all solution. It requires strong leadership, sponsorship, and active participation across departments. Developing a customized scorecard can be time-consuming because there is no single template. The abundance of interpretations and case studies can be overwhelming for newcomers.

Some critics argue that the original approach overlooks stakeholders beyond customers and owners and may underemphasize supply chain partners and employees. Finally, if implemented rigidly, it can seem bureaucratic and may not suit fast-changing industries.

Balanced Scorecard and Project Management

Projects are vehicles for strategy. The BSC helps project managers ensure that every project advances organizational goals. There are three main connections between the BSC and project management:

- BSC development as a project. Creating and implementing a balanced scorecard often requires a cross-functional project. It involves defining perspectives, selecting KPIs, mapping a strategy, and engaging stakeholders. This initiative benefits from formal project management skills.

- Projects to achieve strategic goals. Once a scorecard is in place, projects become the means to realize strategic objectives. Innovations, product launches, process improvements, and organizational changes translate into projects guided by scorecard measures.

- Aligning projects with the scorecard. The most common use of the BSC in project management is linking project objectives to scorecard goals. The Project Management Institute advises aligning projects with organizational strategy, which often includes BSC measures. When a project’s financial, customer, process, and learning goals mirror those of the organization, success becomes easier to measure.

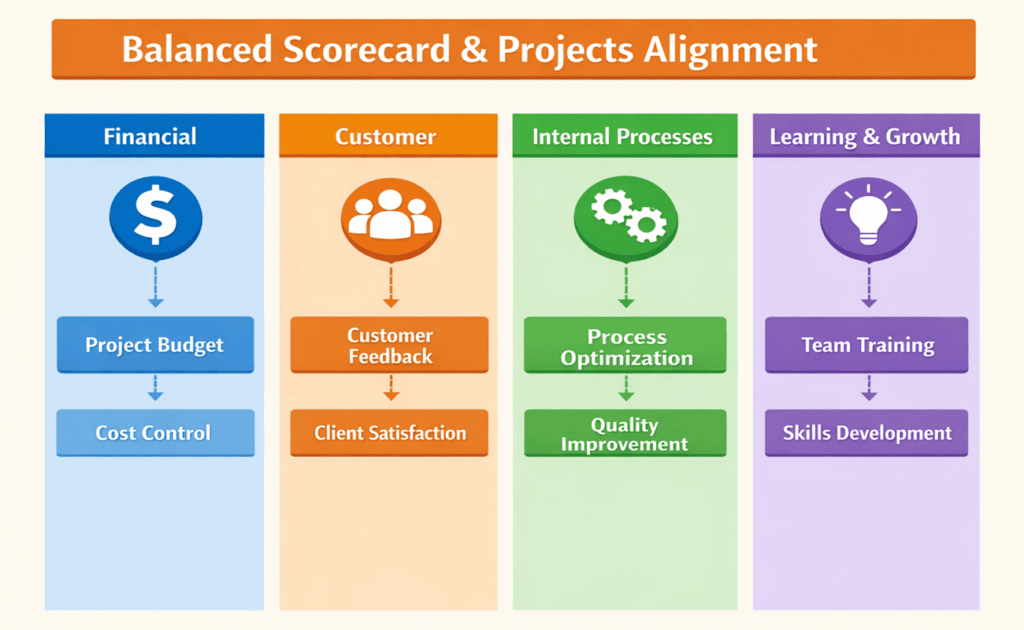

Linking Project Activities to Scorecard Perspectives

The table below shows how common project management activities align with each perspective.

| Perspective | Example project activities |

| Financial | Budget management, cost control, and benefit realization |

| Customer | Stakeholder engagement, requirement gathering, and customer satisfaction tracking |

| Internal Processes | Process mapping, quality management, and resource optimization |

| Learning & Growth | Team training, lessons learned, knowledge sharing |

The following infographic visualizes these connections:

In practice, a project charter should reference the relevant scorecard objectives. For example, if a balanced scorecard aims to reduce process cycle time (internal perspective) by 20 %, a project might focus on automating tasks. Success metrics would then track cycle times before and after implementation.

Emerging Trends and the Future of the Balanced Scorecard

The business world is changing rapidly. New technology, social expectations, and global challenges are reshaping how organizations measure performance. A 2024 article notes that modern Balanced Scorecards are expanding to include data-driven decision-making, agility, digital transformation, and sustainability.

Some key trends include:

- Data-driven management. Companies are using big data and analytics to improve strategic decisions. Real-time dashboards allow managers to predict outcomes and adjust projects quickly.

- Agile and flexible strategies. Traditional long-range plans are giving way to adaptive approaches that respond to market changes. Agile project management fits well with this trend.

- Digital transformation. Digital tools improve communication and performance monitoring. They enable remote teams to coordinate and share data in real time.

- Sustainability and ethics. Organizations are integrating ESG metrics into their scorecards. Examples include Unilever’s Sustainable Living Plan and Patagonia’s commitment to eco-friendly products, which show that sustainable practices can boost financial and non-financial performance.

- Customization and personalization. Future scorecards will be tailored to each organization’s unique needs. This flexibility ensures relevance across industries and sizes.

These trends highlight that the Balanced Scorecard remains a living framework. By embracing digital tools and ESG metrics, organizations ensure their scorecards stay relevant and effective.

Implementing a Balanced Scorecard in Project Management

To integrate the Balanced Scorecard into your project practice, follow these steps:

- Clarify vision and strategy. Define the mission, vision, and strategic objectives. Ensure leadership agreement and communicate these goals to the team.

- Develop a strategy map. Identify cause-and-effect relationships between objectives across the four perspectives. This map will guide project selection and priorities.

- Select meaningful KPIs. For each objective, choose indicators that are measurable, relevant, and controllable. Avoid measuring everything; focus on what drives success.

- Align projects with objectives. Review the project portfolio and ensure each project supports at least one strategic goal. Document the linkage in the project charter and plan.

- Communicate and train. Explain the scorecard and its measures to project teams. Provide training on how to track and report KPIs.

- Monitor and adjust. Use dashboards and regular reviews to track progress. Adjust projects or objectives when necessary. Capture lessons learned and feed them back into the scorecard.

By following these steps, managers create a continuous feedback loop between strategy and execution. Each project becomes a strategic investment rather than a stand-alone endeavor.

FAQs

Q1. What are the four perspectives of the Balanced Scorecard?

The four perspectives are financial, customer, internal processes, and learning and growth. Together, they provide a balanced view of organizational performance.

Q2. How does the Balanced Scorecard help project managers?

It links each project to strategic objectives and KPIs. This alignment improves decision-making, resource allocation, and accountability.

Q3. Can small businesses use a Balanced Scorecard?

Yes. Smaller organizations can scale the framework to fit their needs by focusing on a few key objectives and measures across the four perspectives.

Summary

The Balanced Scorecard is a powerful tool for connecting project execution with business strategy. Balancing financial results with customer value, internal efficiency, and team growth, it helps project managers make better decisions and deliver lasting benefits. When used correctly, the Balanced Scorecard improves alignment, visibility, and accountability across projects. It ensures that every project contributes to long-term organizational success, not just short-term delivery targets.

Further Readings:

Reference:

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.