A fixed-price contract is one of the most popular contracts used in project management. This contract provides peace of mind to buyers and sellers. The seller is mindful of the scope of work, and the buyer can take confidence that the price is firm.

In today’s blog post, I will explain the fixed price contract, its type, examples, and pros and cons.

Let’s get started.

What is a Fixed-Price Contract?

A fixed-price contract is an agreement where the buyer and seller agree on a fixed price for a specific scope of work, regardless of the actual costs incurred. The seller is responsible for any cost overruns. This contract is useful when the scope of work is well-defined. In this contract, the buyer has fewer risks; however, it places the financial risk on the seller if costs exceed expectations.

Government agencies mostly use this contract. Multiple bidders bid for the contract, and the buyer picks the best offer with the lowest quote. Fixed-price contracts have high costs because the seller adds contingencies for risks.

With no hidden costs, buyers don’t have to worry about auditing invoices. The buyer does not know the seller’s profit in a fixed-price contract.

If the scope is not well defined, disputes and claims can creep up, affecting the work’s quality. An undefined scope can cause cost overruns and delays. Any additional work costs more than the normal price of planned work.

Fixed price contracts are less likely to be used in software development projects where the scope changes more often.

Fixed-price contracts are also known as lump-sum contracts, fixed-sum contracts, fixed-price agreements, etc.

Types of Fixed-Price Contracts

A fixed price contract can be of the following types:

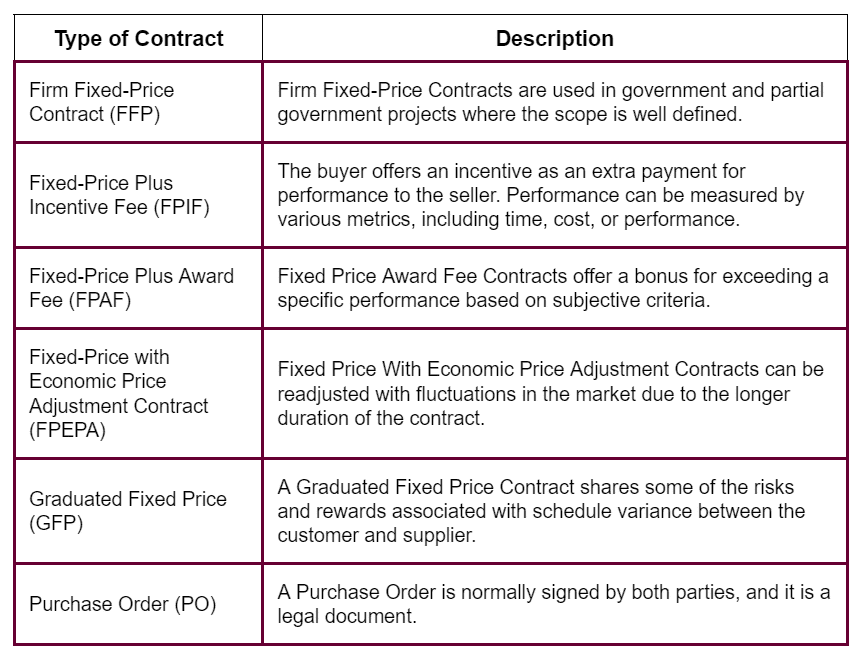

1. Firm Fixed Price Contract (FFP)

A firm fixed price (FFP) contract is an agreement in which the seller agrees to complete the task or deliver specified goods or services at a set price, regardless of the costs incurred. Here, the seller has the maximum risk and minimal risk on the buyer, as the price is fixed and not subject to adjustment based on the seller’s actual costs. FFP contracts are used when requirements are well-defined.

Example: The seller must complete the project for 1,100,000 USD per the defined requirements.

2. Fixed-Price Plus Incentive Fee Contract (FPIF)

A Fixed-Price Plus Incentive Fee (FPIF) contract combines a fixed price with an incentive based on performance. The buyer agrees to pay a fixed amount, while the seller can earn an additional fee if specific performance targets, such as cost savings or early delivery, are met. This contract balances risk by providing the seller a stable payment while motivating them to exceed predefined goals, benefiting both parties through shared gains.

Example: The project cost is 1,100,000 USD. If the project is finished one month early, the seller receives an additional 10,000 USD, incentivizing the seller to work faster.

3. Fixed-Price Plus Award Fee (FPAF)

A Fixed-Price Plus Award Fee (FPAF) contract includes a fixed price for the work and an award fee based on the buyer’s subjective evaluation of the seller’s performance. Unlike incentive fees tied to specific metrics, the award fee is discretionary and depends on the seller’s performance, such as quality, responsiveness, or innovation. This contract motivates sellers to exceed expectations, as the award fee is earned based on the buyer’s satisfaction with the work.

Example: The total project cost is 100,000 USD. If the performance exceeds the planned level, the seller is awarded an additional 5,000 USD.

[This is like the Fixed-Price Incentive Fee (FPIF) contract, except in FPIF, the criteria are objective and outlined in the terms and conditions. In contrast, the award fee is purely a subjective criterion decided by the buyers.]

4. Fixed-Price with Economic Price Adjustment Contract (FPEPA)

A Fixed-Price with economic price adjustment (FPEPA) contract allows for price adjustments based on specified economic conditions, such as inflation, labor costs, or material prices. If certain triggers are met, adjustments are made while the base price is fixed, protecting both buyer and seller from market changes. FPEPA contracts are used in long-term projects where economic fluctuations can affect the prices.

Example: The project’s total cost is 1,100,000 USD, but based on the Consumer Price Index, a price increase of 5% per year will be allowed.

5. Graduated Fixed Price

A Graduated Fixed Price contract sets a fixed price for the work but includes graduated payment levels based on performance. If the seller meets or exceeds the target performance, they receive the full fixed price. If they fall short, the payment is reduced according to predefined tiers. This contract type incentivizes sellers to perform well while allowing buyers to mitigate risk by reducing payments for subpar performance, thus aligning financial outcomes with project success.

Example: 110 USD/hour is paid if the project is finished early. If a project is finished on time, 100 USD/hour is paid. If a project is finished late, 90 USD/hour is paid.

6. Purchase Order

A purchase order (PO) is a formal document issued by a buyer to a seller specifying the types, quantities, and agreed prices for products or services. It serves as a legal offer to purchase and becomes a binding contract once accepted by the seller. POs streamline procurement processes, providing clear terms and documentation for both parties. They are commonly used in commodity procurement.

Example: Buy 50 LED lights at 6 USD per piece.

Mathematical Examples of Fixed-Priced Contracts

Before we examine the following equations, let us understand a few procurement terms.

Price: This is the amount the seller charges the buyer.

Profit (fee): The amount the seller earns after the cost.

Target Price: This compares the result (final price) with what was expected (target price).

Sharing Ratio: This is expressed in a ratio such as 80/20. This ratio describes how cost savings or cost overruns are shared between buyer and seller. The first number represents the buyer portion, and the second represents the seller portion.

Ceiling Price: This is the highest price the buyer will pay. If any additional costs are incurred, the seller will have to absorb them, which ensures the seller is motivated to control costs.

Point of Total Assumption (PTA): This term is used only in fixed-price incentive fee costs. This is the amount above which the seller bears all cost overruns.

PTA = ( (Ceiling Price – Target Price)/Buyer’s Share Ratio) + Target Cost

Example – 1

Target Cost of Project = 60,000 USD; seller’s fee = 15,000 USD; ceiling price = 100,000 USD; ratio is 60:40; Actual Cost = 120,000 USD. Calculate the seller’s profit or loss.

Target Price = Target Cost + Seller’s Fee = 75,000 USD.

PTA = ((100,000-75,000)/0.6) + 60,000 = 41,667 + 60,000 = 101,677.

At or above PTA, the contract price is fixed and is equal to the ceiling price.

As the Actual Cost is 120,000 USD, but the PTA is 101,677, and the ceiling price is 100,000, and all costs above 100,000 will be borne by the seller (-20,000 USD).

Here is a more detailed explanation of the seller’s profit/loss:

Cost Overrun = Actual Cost – Target Cost = 120,000 – 60,000 = 60,000

Buyer’s share of Cost overrun = Buyer’s ratio * cost overrun = 0.6 * 60,000 = 36,000

Seller’s share of Cost overrun = seller’s ratio * cost overrun = 0.4 * 60,000 = 24,000

Buyer’s price = Target Price + Buyer’s share (or) Ceiling Price, whichever is lower; 75,000 + 36,000 = 111,000 or Ceiling Price of 100,000, whichever is lower.

Thus, the Buyer’s price = 100,000.

Seller’s Profit/Loss = Buyer’s price – Actual Costs = 100,000 – 120,000 = -20,000 USD.

Example – 2

Target Cost of Project = 60,000 USD; seller’s fee = 15,000 USD; ceiling price = 100,000 USD; ratio is 60:40; Actual Cost = 101,667 USD. Calculate the seller’s profit or loss.

Target Price = Target Cost + Seller’s Fee = 75,000 USD.

PTA = ((100,000-75,000)/0.6) + 60,000 = 41,667 + 60,000 = 101,667.

In this case, PTA is equal to the Actual Cost, which is above the ceiling price, but the buyer will pay only the ceiling price.

As the Actual Cost is 101,667 USD, PTA is 101,667, and the ceiling price is 100,000, all costs above 100,000 will be borne by the seller (-1,667 USD).

A more detailed explanation of the seller’s profit/loss:

Cost Overrun = Actual Cost – Target Cost = 101,667 – 60,000 = 41,667

Buyer’s share of Cost overrun = Buyer’s ratio * cost overrun = 0.6 * 41,667 = 25,000

Seller’s share of Cost overrun = seller’s ratio * cost overrun = 0.4 * 41,667 = 16,667

Buyer’s price = Target Price + Buyer’s share (or) Ceiling Price, whichever is lower; 75,000+25,000 = 100,000 or Ceiling Price of 100,000, whichever is lower.

Therefore, the Buyer’s price = 100,000.

Seller’s Profit/Loss = Buyer’s price – Actual Costs = 100,000 – 101,667 = -1,667 USD.

In the two examples above, when actual costs equal or exceed the point of total assumption, the buyer pays only the ceiling price, which the seller must pay out of pocket.

Example – 3

Target Cost of Project = 60,000 USD; seller’s fee = 15,000 USD; and ceiling price = 100,000 USD; ratio is 60:40; Actual Cost = 100,000 USD. Calculate the seller’s profit or loss.

Target Price = Target Cost + Seller’s Fee = 75,000 USD.

PTA = ((100,000-75,000)/0.6) + 60,000 = 41,667 + 60,000 = 101,677.

The Actual Cost is equal to the Ceiling Price. In this case, will the seller still be at a loss? Let’s dive in further to understand.

Cost Overrun = Actual Cost – Target Cost = 100,000 – 60,000 = 40,000

Buyer’s share of Cost overrun = Buyer’s ratio * cost overrun = 0.6 * 40,000 = 24,000

Seller’s share of Cost overrun = seller’s ratio * cost overrun = 0.4 * 40,000 = 16,000

Buyer’s price = Target Price + Buyer’s share (or) Ceiling Price, whichever is lower; 75,000 + 24,000 = 99,000 or 100,000, whichever is lower. So, the Buyer’s price = 99,000.

Seller’s Profit/Loss = Buyer’s price – Actual Costs = 99,000 – 100,000 = 1,000 USD.

Accordingly, sellers can be in the red (even before hitting the point of total assumption) when Actual Costs are equal to the Ceiling Price because of the sharing ratio.

The three examples above show that the seller is at a loss and didn’t get the fees. So, when does the seller get his fees in full as expected? This is set in motion when the actual cost is the same as the target cost, even if the seller cuts his profit margins or absorbs losses, as explained previously.

Let’s consider another example where the actual cost is the same as the target costs.

Example – 4

Target Cost of Project = 60,000 USD; seller’s fee = 15,000 USD; ceiling price = 100,000 USD; ratio is 60:40; Actual Cost = 60,000 USD. Calculate the seller’s profit or loss.

Target Price = Target Cost + Seller’s Fee = 75,000 USD

PTA = ((100,000-75,000)/0.6) + 60,000 = 41,667 + 60,000 = 101,677.

Cost Overrun = Actual Cost – Target Cost = 60,000 – 60,000 = 0

Buyer’s share of Cost overrun = Buyer’s ratio * cost overrun = 0.6 * 0 = 0

Seller’s share of Cost overrun = seller’s ratio * cost overrun = 0.4 * 0 = 0

Buyer’s price = Target Price + Buyer’s share (or) Ceiling Price, whichever is lower; 75,000 + 0 = 75,000 or 100,000, whichever is lower. So, the Buyer’s price = 75,000.

Seller’s Profit/Loss = Buyer’s price – Actual Costs = 75,000 – 60,000 = 15,000 USD.

In this case, sellers will get their full fees when the actual cost equals the target cost, and the buyer will pay the target price as expected.

With fixed-price contracts, sellers are motivated to monitor costs to avoid cost overruns or losing money.

When Should I Use the Fixed Price Contract?

In the following cases, you can use the fixed-price contract:

- Clear Scope and Requirements: When the project scope, objectives, and deliverables are clearly defined, there is little uncertainty about what must be done. This allows both parties to agree on a fixed price upfront.

- Low Risk of Changes: Fixed-price contracts work well when there is a low chance of changes in project scope, requirements, or other variables that could impact costs. They also work well when the work is straightforward and not subject to significant changes.

- Well-Defined Timeline: When the project has a well-defined timeline and schedule that is unlikely to change, making it easier to estimate costs accurately.

- High Confidence in Cost Estimates: When the seller can confidently estimate the project’s cost based on experience, historical data, or clear specifications.

- Buyer Preference for Cost Certainty: When the buyer prefers cost certainty and wants to avoid the risk of cost overruns. This can be especially important for projects with tight budgets.

- Experienced Vendors: When working with experienced contractors with a track record of delivering similar projects on time and within budget, they are more likely to provide accurate estimates and manage risks effectively.

- Regulatory or Compliance Requirements: Sometimes, fixed-price contracts are required by regulations, industry standards, or internal policies, particularly in government or public-sector projects.

Fixed-Price Vs Cost-Plus Contracts

Fixed price and cost plus are different contracts.

In a fixed-price contract, the scope of work is well-defined and fixed. The seller must complete the task within an agreed-upon price and duration.

In a cost-plus contract, the scope of work is not defined. The seller must complete the task as instructed by the buyer, and they will receive the cost they spent plus a fee as mentioned in the contract. The cost-plus contract has a flexible duration.

The risk is on the seller in a fixed-price contract and on the buyer in a cost-plus contract.

In a fixed-price contract, the seller spends less time reviewing the invoice, while in a cost-plus contract, they meticulously check the invoice for any inflated costs, as the seller gains a profit from the higher rates.

Fixed Price Vs Time and Material Contracts

In a T&M contract, the buyer pays the seller based on the time spent and materials used for the work, with agreed-upon hourly rates and material costs. This contract is flexible and suitable for tasks where the scope is not well-defined or may evolve, allowing adjustments as the project progresses. The risk is on the buyer, who bears the cost of any overrun.

A fixed-price contract sets a price for the project regardless of the time and materials used. The seller assumes more risk, as they must deliver the project within the agreed budget. FP contracts are best for well-defined requirements. They provide cost certainty for the buyer but less flexibility if the project scope changes.

Pros of Fixed Price Contracts

- Cost Certainty: The buyer knows the total cost upfront, simplifying budgeting and financial planning.

- Minimal Buyer Risk: The seller assumes the risk of cost overruns, as the price is fixed regardless of actual expenses.

- Clear Scope: Fixed price contracts require a well-defined project scope, reducing ambiguity and potential disputes.

- Seller Incentive: Sellers are motivated to control costs and complete the project efficiently to maximize their profit margin.

Cons of Fixed Price Contracts

- Inflexibility: Any changes to the project scope or unforeseen challenges may require costly amendments, leading to delays.

- Higher Initial Costs: Sellers may inflate the price to cover potential risks, leading to higher upfront costs for the buyer.

- Quality Risks: Sellers might cut corners to stay within budget, potentially compromising quality.

- Longer Negotiation: Determining a fair fixed price requires detailed negotiations, which can delay project start times.

Conclusion

Fixed-price contracts offer buyers cost certainty and minimal financial risk, making them ideal for well-defined projects with clear requirements. Fixed-price contracts remain popular in project management for their simplicity and predictability. Careful planning, clear scope definition, and thorough negotiation are key to successfully leveraging this contract type in various industries.

You should choose a fixed-price contract if the scope is well defined, time is limited to monitor work, and there is a low chance of changes in the scope of work.

Further Readings:

- What is a Contract?

- What is Project Procurement Management?

- What are the Types of Procurement Contracts?

- What is a Firm Fixed-Price Contract?

- What is a Time & Material Contract?

References:

This topic is important from a PMP exam point of view.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.