Managing project costs is a key challenge in modern project management. The point of total assumption (PTA) plays a critical role in fixed-price incentive-fee contracts by defining the cost limit at which the seller assumes full responsibility. Understanding the point of total assumption helps you control risks and avoid unexpected losses.

In PTA project management, this concept ensures a fair balance between buyer and seller. By learning the PTA formula and its practical applications, you can make better financial decisions, improve contract performance, and effectively reduce cost overruns in complex projects.

Understanding the Point of Total Assumption

An FPIF contract sets a target cost, target profit, and a ceiling price. The target cost represents the agreed-upon budget for the seller’s work, while the target profit (sometimes called the target fee) is the reward the seller expects for meeting the budget. The ceiling price caps the buyer’s total payment; any spending beyond this ceiling is the seller’s responsibility.

The Point of Total Assumption (PTA) is the cost level at which the seller assumes full responsibility for any additional expenses. Before reaching PTA, cost overruns are shared between buyer and seller according to an agreed-upon sharing ratio. At PTA and beyond, the sharing ratio shifts to 0/100, meaning the seller assumes all additional costs. This mechanism protects the buyer and encourages the seller to control costs.

Why PTA Matters Today

The Point of Total Assumption (PTA) is important because it defines the exact cost point at which the seller assumes full financial responsibility for overruns in a fixed-price incentive-fee contract. It protects the buyer from unlimited cost exposure while encouraging the seller to control expenses. PTA creates a clear risk boundary, which improves cost discipline and accountability. It also helps both parties negotiate fair sharing ratios and pricing structures.

By understanding PTA, you can reduce financial risks, improve contract performance, and ensure better cost control, making it a critical concept in effective project management.

Key Terms and Concepts

Before calculating PTA, it helps to understand the terms used in FPIF contracts:

- Target Cost: The cost that the buyer and seller agree is reasonable for the work. Estimates rely on historical data and expert judgment.

- Target Profit (Target Fee): The profit the seller expects to earn if the project finishes at the target cost.

- Target Price: The sum of the target cost and target profit. This amount represents what the buyer plans to pay if costs stay on track.

- Actual Cost: The amount the seller spends while performing the work.

- Ceiling Price: The maximum amount the buyer will pay for the job. Costs beyond this point come out of the seller’s pocket.

- Sharing Ratio: The ratio that determines how cost overruns or underruns are shared between buyer and seller before reaching PTA. A 70/30 ratio means the buyer bears 70% of the cost overrun and the seller 30%.

- Profit Adjustment: The change in the seller’s profit based on how actual costs compare to the target cost. Profit shrinks when costs rise and grows when costs fall.

The PTA Formula

The Point of Total Assumption is calculated using the following formula:

Here, the buyer’s share is the buyer’s portion of the sharing ratio, expressed as a decimal (70% becomes 0.70). The formula shows that PTA depends on how far the ceiling price sits above the target price and how much cost risk the buyer is willing to absorb. The seller’s profit starts to erode once actual costs surpass the PTA.

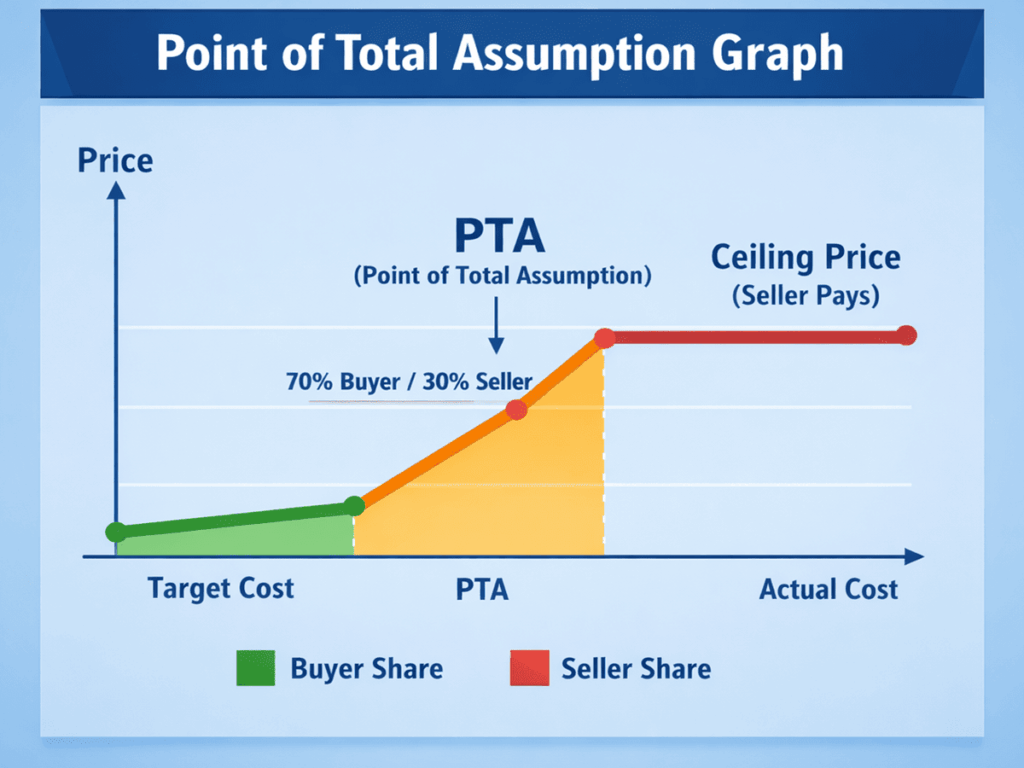

Visualizing the Point of Total Assumption

To better understand how the PTA works, look at the graph below. The y-axis represents the price paid, and the x-axis shows the actual cost. The line initially rises gently up to the target cost. Between the target cost and the PTA, cost overruns are shared (the slope reflects the sharing ratio).

Beyond the PTA, the line becomes flat because the buyer stops covering additional costs, such as any spending past this point, which reduces the seller’s profit until reaching the ceiling price, where payments stop entirely.

PTA Example Calculations

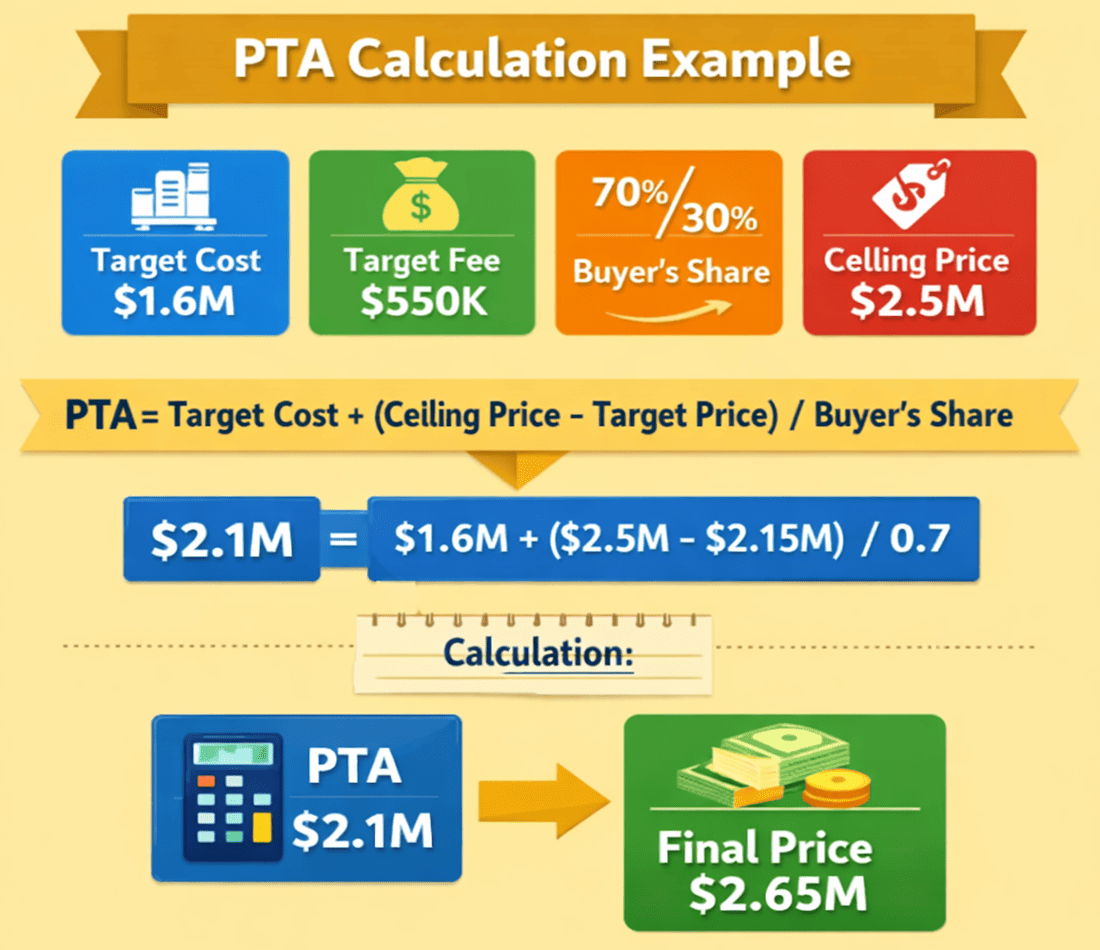

Example 1

Suppose an FPIF contract has these terms:

- Target Cost: USD 1.6 million

- Target Fee (Profit): USD 550,000

- Buyer’s Sharing Ratio: 70/30 (buyer/seller)

- Ceiling Price: USD 2.5 million

First, calculate the target price:

Target Price = Target Cost + Target Fee

= 1,600,000 + 550,000

= 2,150,000 USD

Next, apply the PTA formula:

PTA =1,600,000 + (2,500,000 – 2,150,000) / 0.70

= 1,600,000 + 350,000 / 0.70 = 1,600,000 + 500,000

= 2,100,000 USD

Finally, calculate the resulting price that the buyer would pay if costs reach PTA:

Resulting Price = PTA + Target Fee = 2,100,000 + 550,000 = 2,650,000 USD

Notice that the resulting price exceeds the ceiling price (USD 2.5 million). Since the buyer has capped the payment at the ceiling, the seller will receive no more than USD 2.5 million, and any further costs will cut into the seller’s profits.

Example 2

Consider a larger project with the following values:

- Target Cost: USD 3.5 million

- Target Fee: USD 650,000

- Buyer’s Sharing Ratio: 70/30

- Ceiling Price: USD 5 million

- Actual Cost: USD 4.8 million

First, determine the profit (shrink) or overrun:

Profit = Target Cost – Actual Cost

= 3,500,000 – 4,800,000

= -1,300,000 USD (a budget overrun)

The seller’s share of this overrun is 30% of USD 1.3 million, or – USD 390,000. The adjusted profit (target fee plus profit shrink) is:

Adjusted Profit = 650,000 – 390,000 = 260,000 USD

Thus, the final contract price (actual cost + adjusted profit) would be:

Final Price = 4,800,000 + 260,000 = 5,060,000 USD

Because this exceeds the ceiling price of USD 5 million, the buyer still pays only the ceiling price. Any further cost growth is the seller’s burden.

Advantages of PTA

Employing the Point of Total Assumption clause in FPIF contracts provides several benefits:

- Encourages cost control: Knowing that cost overruns beyond PTA will eat into their profits, sellers are motivated to manage resources efficiently. This alignment of incentives often leads to tighter cost monitoring and fewer surprises.

- Protects buyers’ budgets: By capping the buyer’s liability at the ceiling price, PTA limits the buyer’s cost exposure. This is especially valuable in government or large capital projects where taxpayer money is at stake.

- Improves contract negotiations: PTA provides a clear cost boundary, making it easier for both parties to discuss risk allocation. Contractors can adjust their bids and share ratios based on their appetite for risk and potential reward.

- Supports project transparency: With a structured sharing ratio and clear thresholds, both parties understand how changes in costs affect profit. This reduces disputes and helps maintain trust.

PTA Limitations and Considerations

While PTA is a valuable tool, it is not a cure-all. Consider the following challenges:

- Unforeseen risks: External factors such as economic shocks, supply chain disruptions, or technical issues may push costs beyond PTA despite diligent planning. Contractors may still face losses when risks are beyond their control.

- Potential for conflict: Disagreements may arise about what constitutes allowable costs or who is responsible for overruns. Clear contract language and open communication are essential.

- Profit margins at risk: For contractors, the PTA is a line in the sand—beyond it, profit erodes rapidly. Contractors must carefully evaluate their risk tolerance before agreeing to the sharing ratio and ceiling price.

- Need for accurate cost tracking: PTA clauses require a reliable accounting system and timely cost reporting. Without accurate data, it is difficult to know when the project is approaching PTA.

FAQs

Q1. What is the difference between a target cost and a ceiling price?

The target cost is the agreed-upon estimate to complete the work, whereas the ceiling price is the maximum amount the buyer will pay. Costs above the ceiling come out of the seller’s pocket.

Q2. Why would a contractor agree to a PTA clause?

Contractors accept PTA clauses in exchange for potential incentives. If they control costs and finish under budget, they earn a higher profit. The clause also clarifies risk sharing, which can help win bids.

Q3. How does the sharing ratio affect PTA?

A higher buyer share (such as 80%) increases the PTA, giving the seller more room before profits decline. A lower buyer share accelerates the seller’s assumption of cost overruns.

Q4. Can PTA apply to time overruns?

PTA specifically addresses cost overruns, not schedule delays. However, schedule slips often cause cost increases, so managing time effectively helps avoid hitting PTA.

Q5. When should a fixed-price incentive contract be used?

FPIF contracts are ideal when the scope is defined, but execution is uncertain. They encourage sellers to innovate and deliver efficiently without exposing buyers to unlimited cost risk.

Summary

The Point of Total Assumption is a vital concept in fixed-price incentive-fee contracts that helps balance risk between buyers and sellers. It sets a clear limit where the seller becomes fully responsible for cost overruns, encouraging strong cost control. By understanding the PTA formula and its impact, you can make better decisions, negotiate smarter contracts, and reduce financial risks. Applying PTA effectively leads to improved project performance and more predictable cost outcomes.

Understand the Point of Total Assumption (PTA) in fixed-price incentive fee contracts. Learn formulas and examples to control project costs.

Further Readings:

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.