Understanding the APR Vs APY difference is essential when comparing loans, credit cards, and savings accounts. These two rates may look similar, but they serve very different purposes. APR shows the yearly cost of borrowing, including interest and certain fees, while APY reflects the total interest you earn on savings after compounding. Knowing how each works helps you avoid costly mistakes and make better financial decisions.

Whether you are taking out a loan or growing your savings, understanding the difference between APR and APY helps you choose the option that best supports your financial goals.

In today’s blog post, I will explain the annual percentage rate and the annual percentage yield, and how they differ.

Key Takeaway

- APR measures borrowing costs. It combines the interest rate with certain loan fees and excludes compounding.

- APY measures what you earn. It reflects the effect of compounding on your savings or investment returns.

- Compounding widens the gap. More frequent compounding results in a higher APY than APR at the same nominal rate.

- Average rates vary widely. Federal Reserve data show credit card APRs averaged around 20.97% in late 2025, while FDIC data report an average savings APY of 0.39% in March 2026.

- Compare apples to apples. Use APR to compare loans and APY to compare savings products; mixing the two leads to confusion.

What is Annual Percentage Rate (APR)?

An annual percentage rate tells you how much you will pay to borrow money over a year. It includes the interest rate and certain fees, such as mortgage points, broker charges, and other closing costs. APR gives borrowers a more complete view of the cost of a loan than a simple interest rate does. However, APR does not factor in compounding; if you carry a balance from month to month, interest accrues on top of interest, which can drive the effective cost higher.

In practice, credit card issuers and lenders must disclose the APR under the Truth in Lending Act. This requirement ensures that you can compare offers across banks and lenders. The CFPB explains that the APR represents the interest rate plus any additional fees charged by the lender. Because lenders calculate APR differently depending on the product, look closely at what fees are included.

The basic formula for APR is:

Where “Fees” are the total loan fees, “Interest” is the total interest paid, “Principal” is the loan amount, and n is the number of days in the loan term. Although you don’t need to crunch this formula yourself, understanding that fees raise the APR helps you spot expensive loans.

What is Annual Percentage Yield (APY)?

An annual percentage yield measures how much interest your deposit will earn over a year after taking compounding into account. Banks and credit unions disclose APY on certificates of deposit (CDs), savings accounts, and money-market accounts. The more often interest is compounded, monthly, quarterly, or daily, the higher the APY will be. Unlike APR, APY does not include fees, but federal law requires deposit-taking institutions to disclose APY so you can shop around.

The formula for APY looks more complex because it captures compounding:

Here r is the periodic rate (the nominal rate divided by the number of compounding periods), and n is the number of compounding periods per year. If your savings rate is 5% and interest compounds monthly, r = 0.05/12 and n = 12. Plugging those numbers into the formula yields an APY of roughly 5.116%, which is higher than the nominal rate because of compounding.

How Compounding Changes the Rate

Compounding occurs when the interest you earn or owe is added to the principal, so you earn or pay interest on that interest. Because APR ignores compounding, the effective cost of borrowing can be higher than the quoted APR when interest compounds more than once a year. Similarly, the effective return on your savings (APY) increases with more frequent compounding.

Example: Credit Card Vs High-Yield Savings Account

Imagine you have a $2,000 credit card balance with an 18% APR. If you only make minimum payments and carry the balance for a year, you could pay around $360 in interest, depending on your repayment pattern. Since interest compounds daily, the actual cost may be even higher.

Now, consider putting $2,000 into a high-yield savings account offering 4.5% APY. With compounding, you would earn about $90 in interest over a year.

This example shows how APR increases what you pay, while APY increases what you earn.

The Impact of Compounding on Borrowing

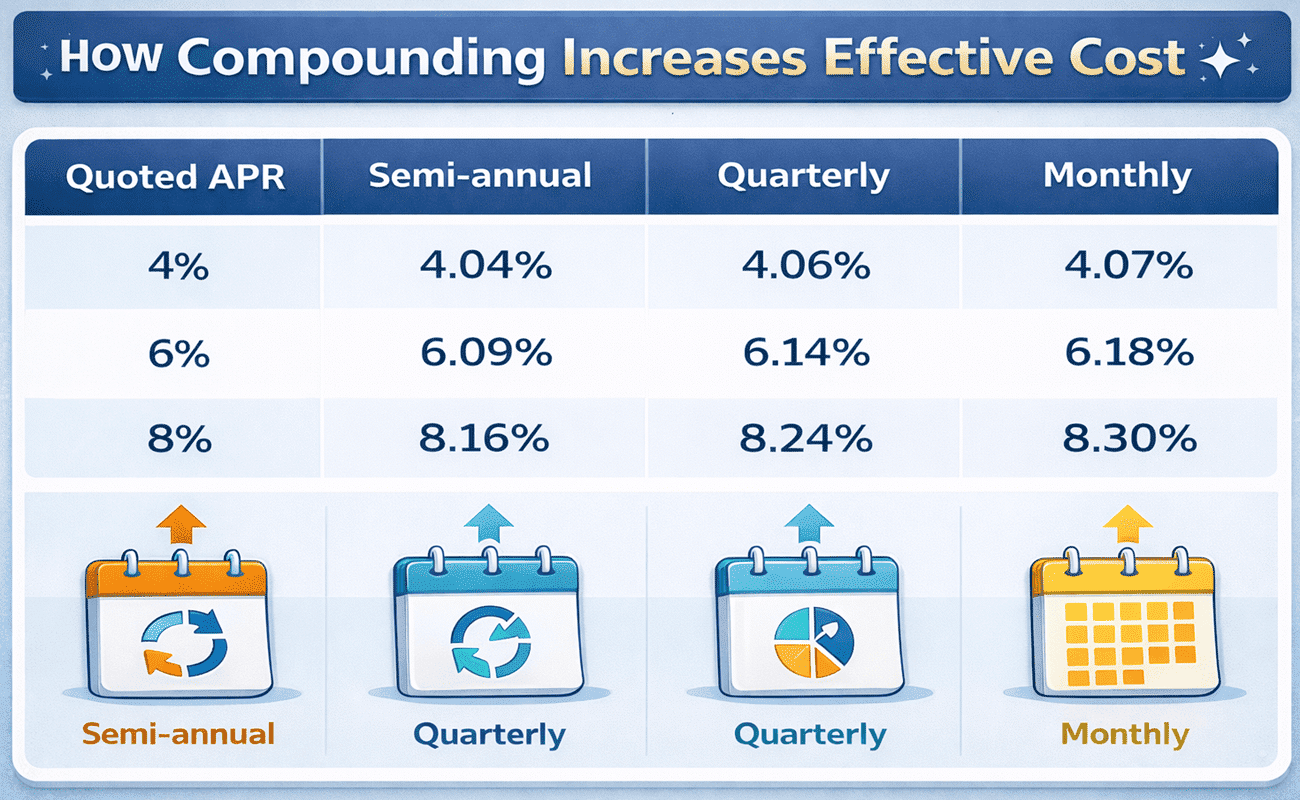

Banks often advertise APRs without explaining how compounding affects what you actually pay. Consider the table below, which shows three quoted APRs and the corresponding effective rates when interest is compounded semi-annually, quarterly, or monthly. The more frequent the compounding, the higher the effective cost.

For example, a 4% APR becomes 4.07% when interest compounds monthly, while a 8% APR becomes 8.3%. Over decades on a mortgage, this seemingly small difference can add up.

Borrower’s Perspective

Borrowers want the lowest possible APR. The average credit-card interest rate at U.S. commercial banks reached 20.97% in November 2025, the highest level in decades. However, your actual APR depends on your credit score, income, and the type of loan. A credit union credit card might offer an APR around 15%, while a rewards card may charge more than 23% APR. When comparing loans, look at the APR and ask whether the rate is fixed or variable, whether there are annual fees or points, and whether you can avoid compounding by paying the balance in full each month.

It’s smart to shop around and use online calculators to see how monthly payments and total interest change with different APRs. Always compare APR to APR; mixing APR and APY can be misleading.

Saver’s Perspective

Savers seek the highest possible APY. According to the FDIC’s March 16, 2026, national rates report, the average savings account earned an APY of 0.39%. That’s a baseline figure; many online banks and credit unions offer much higher yields. Because APY includes compounding, it allows you to compare accounts that compound interest on different schedules. When evaluating a CD or savings account, look at the APY, compounding frequency, minimum balance requirements, and any early withdrawal penalties. Even a difference of one-quarter of a percentage point can add up over time.

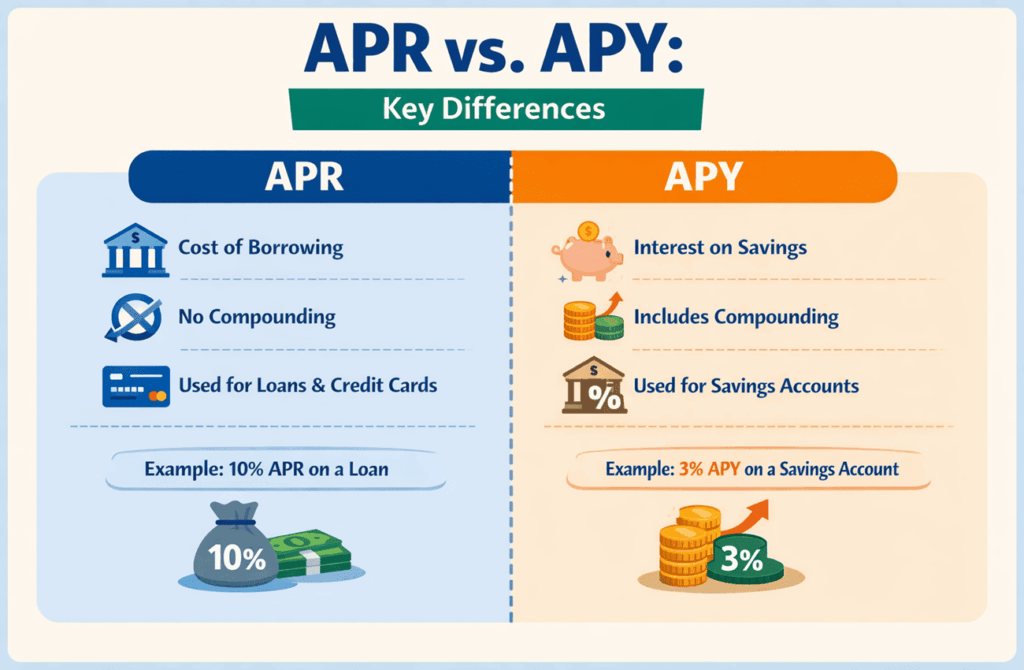

APR Vs APY

The infographic below shows the key differences between APR and APY:

Which Should You Use: APR or APY?

Use APR when comparing loans and credit cards, and APY when comparing savings products. Mixing them leads to bad comparisons. APR shows the annual cost of borrowing, including certain fees, but ignores compounding. APY shows how fast your savings grow with compounding. Think of APR as the price tag on a loan and APY as the yield on your deposit. When you see a loan advertised with a low interest rate, ask about the APR to capture the fees. When you see a savings rate advertised, look for the APY to know the true return.

FAQs

Q1. What is a good APR?

A good APR is simply a low one. Credit-card APRs average around 21%, so anything well below that is competitive. Your personal rate depends on your credit score, income, and debt history, so compare offers and aim for the lowest APR you qualify for.

Q2. How do I calculate APY on my savings account?

Divide the annual rate by the number of compounding periods, add 1, raise the result to the number of periods, and subtract 1. Many banks provide calculators, so you don’t have to do the math yourself.

Q3. Why is APY usually higher than APR at the same nominal rate?

APY accounts for the effect of compounding, which causes money to grow faster. APR ignores compounding, so the effective cost or return will be lower.

Summary

Understanding the difference between APR and APY helps you make smarter financial choices. APR shows the true cost of borrowing, while APY reveals the real return on savings with compounding. Even small differences in rates can significantly impact what you pay or earn over time. By comparing APR for loans and APY for savings, you can avoid costly mistakes and maximize your money. Always review the terms carefully and use a calculator to see how interest affects your finances.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.