Understanding the true cost of borrowing can be confusing. You see a credit card ad promising a low rate, but how do you know what you’ll really pay? The annual percentage rate (APR) answers that question by showing the yearly cost of credit, including interest and certain fees.

This blog post breaks down what APR means, how it’s calculated, why it matters, and how you can use it to save money.

Key Takeaway

- APR shows the annual cost of credit. It includes the nominal interest rate plus many fees, but does not reflect compounding.

- Disclosure is required. The U.S. Truth in Lending Act (TILA) obliges lenders to reveal the APR so that consumers can compare loans on an equal basis.

- APR differs from APY. APR is based on simple interest, while the annual percentage yield (APY) includes the effect of compounding.

- Different products have different APRs. Credit cards may charge separate APRs for purchases, cash advances, and balance transfers, and may impose a penalty APR for late payments. Loans can have fixed or variable APRs.

- APR is rising. In 2024, the average APR on general-purpose credit cards reached 25.2%, while private-label cards averaged 31.3%.

What is Annual Percentage Rate (APR)?

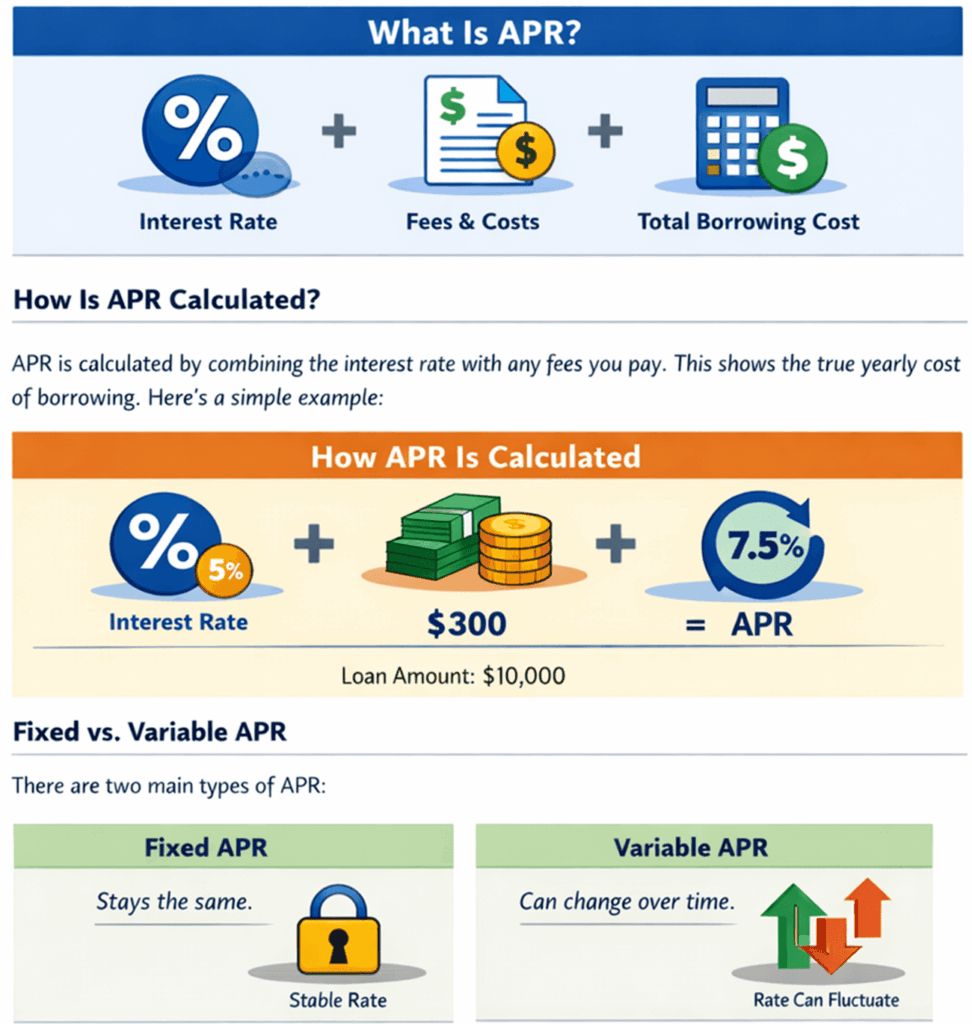

Annual Percentage Rate (APR) is the yearly cost of borrowing money, expressed as a percentage. It includes not only the interest rate but also certain fees, giving a clearer picture of the total cost of a loan or credit. APR helps borrowers easily compare different financial products. Unlike APY, it does not account for compounding. A lower APR means lower borrowing costs.

Lenders are required to disclose APR, making it a key tool for informed financial decisions. Understanding APR helps you choose better loans, manage debt wisely, and avoid paying more than necessary over time.

How APR Works

APR expresses the cost of borrowing as a percentage of the principal. It tells you what portion of the principal you’ll pay each year when monthly payments and certain fees are factored in. Because it excludes compounding, the APR is usually lower than the effective rate you actually pay on a loan that accrues interest daily or monthly. For investments, APR represents the yearly return before compounding, so it can understate total earnings.

Why APR Disclosure Matters

Before 1968, lenders often highlighted low monthly rates while hiding the true annual cost. The Truth in Lending Act changed that by mandating APR disclosure. Without this rule, a company might advertise a very low monthly rate that, when converted to an annual rate, is actually higher than competing offers. A standard disclosure helps consumers compare products on an “apples to apples” basis and discourages misleading marketing.

Types of Annual Percentage Rate

APR isn’t one-size-fits-all. Different financial products use different APR structures, and credit card companies often apply multiple rates to the same account.

Purchase, Cash Advance, and Balance Transfer APRs

Credit card issuers typically charge one APR for everyday purchases, a higher rate for cash advances, and a separate rate for balance transfers from other cards. A penalty APR, often well over 25%, may apply if you miss payments or violate card terms. Many cards also offer an introductory APR of 0% or near zero for a limited time to attract new customers. Once the promotion ends, the standard purchase or balance transfer rate applies.

Fixed Vs Variable APR

Loans and some credit cards may have a fixed or variable APR. Fixed APRs remain stable for the life of the loan or credit facility, making budgeting easier. Variable APRs fluctuate with an underlying benchmark, typically the prime rate, and can rise or fall over time. When interest rates climb, variable APRs may increase, causing borrowers to pay more. Conversely, a variable rate can fall if market rates decline.

APR and Your Credit Score

Your credit history significantly influences the APR a lender offers. People with excellent credit scores tend to qualify for much lower rates than those with average or poor scores. Improving your credit by paying bills on time, keeping balances low, and maintaining a long credit history can help you secure better APRs on credit cards and loans.

APR Vs APY and Nominal Rate

APR and the annual percentage yield (APY) are often confused. APR considers simple interest and some fees; it doesn’t account for compounding. APY measures the effective annual rate after compounding is applied. APY is therefore higher than APR for the same nominal rate when interest compounds more than once per year. Banks often highlight APY for savings products because it appears larger, while lenders emphasize APR when promoting loans.

Example: APR Vs APY

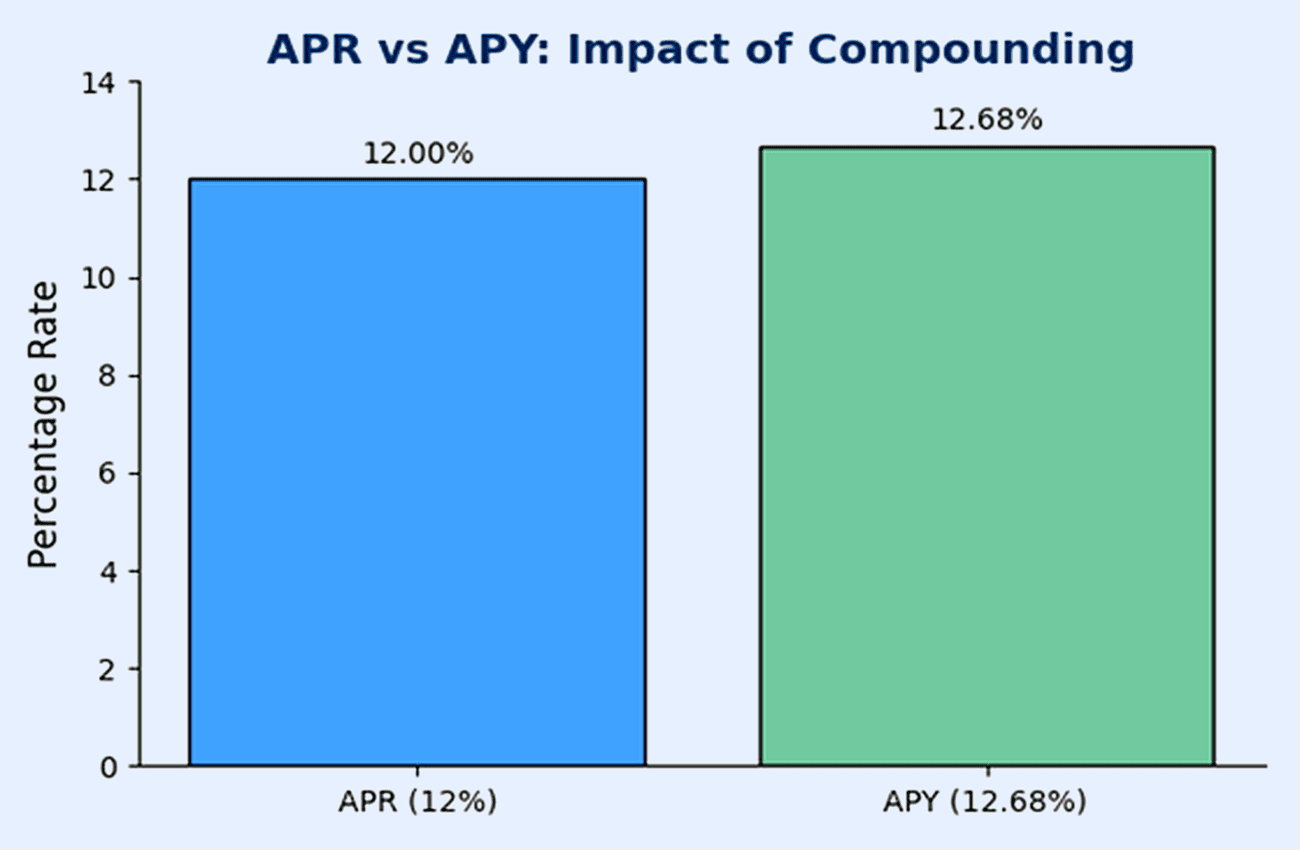

Suppose you borrow $10,000 at 12% APR, with interest compounding monthly. The monthly periodic rate is 1%. After the first month, the balance becomes $10,100. In the second month, interest accrues on the new balance, so the interest payment is $101. Carry this balance for a full year, and the effective interest rate becomes 12.68%, which is the APY. The difference arises because each month’s interest is added to the principal, and subsequent interest calculations include those additions.

The bar chart below visualizes this difference. The APY bar is slightly taller than the APR bar, illustrating how compounding increases the effective rate.

How to Calculate APR

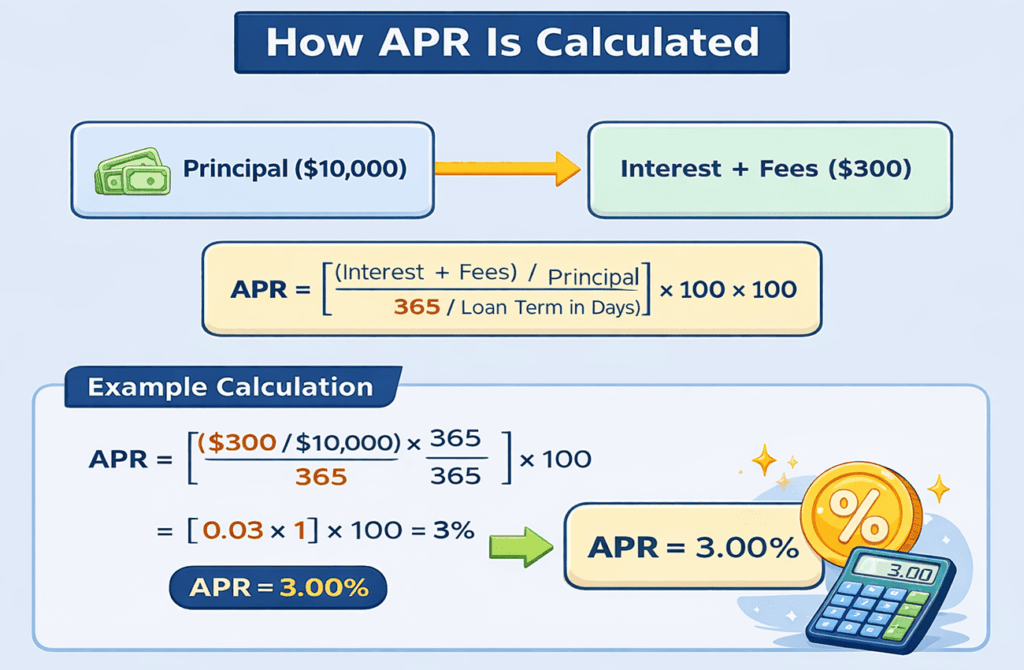

APR is derived from the periodic interest rate, fees, and the length of the loan. The general formula is:

APR = ((Interest + Fees) ÷ Principal) × (365 ÷ Days in Loan Term) × 100

Where:

- Principal is the initial amount borrowed.

- Interest is the total interest paid over the life of the loan.

- Fees include administrative charges, points, and other upfront costs.

- Days in Loan Term is the total number of days between the loan’s start and end.

For example, imagine you borrow $10,000 for one year and pay $300 in interest and fees. Plugging those numbers into the formula yields an APR of 3%:

(($300 ÷ $10,000) × (365 ÷ 365)) × 100 = 3%

Step-by-Step Guide

- Determine the periodic rate. Divide the interest rate by the number of compounding periods in a year.

- Add fees to the total interest. Include points and closing costs that the lender requires.

- Divide by principal. This ratio shows the cost of borrowing relative to the amount financed.

- Annualize the figure. Multiply by 365 and divide by the number of days in the loan term.

- Convert to a percentage. Multiply by 100 to express the result as a percentage.

While the formula looks intimidating, many online calculators will compute APR for you once you input the necessary information.

Pros and Cons of Using APR

Advantages

- Easy comparison: APR simplifies shopping by distilling interest and many fees into a single number, making it easier to compare loans or credit cards.

- Consumer protection: By law, lenders must disclose APR before you sign a contract, helping to prevent misleading advertising.

- Transparency: APR reveals the true cost of credit after accounting for certain fees and charges.

Drawbacks

- No compounding: APR is based on simple interest, so it doesn’t reflect how often interest is added to your balance. As a result, the actual cost of credit may be higher.

- Excluded fees: Some lenders exclude certain costs from the APR calculation. Origination fees, appraisal charges, and other closing costs might not be included.

- Assumes long terms: APR calculations often assume the loan is held to maturity. For short-term loans, the effect of fees may be understated.

- Variable rates: For adjustable-rate mortgages or variable-rate loans, the APR is based on current rates and does not reflect future rate increases.

What is a Good APR?

There is no single “good” APR. A competitive rate depends on market conditions, the prime rate, and your credit score. When the Federal Reserve keeps rates low, lenders may offer introductory APRs of 0% for car loans or credit cards. These enticing deals are sometimes temporary, so always read the fine print. Borrowers with excellent credit (scores above 740 or 760) usually qualify for lower APRs on mortgages and personal loans. If your rate seems high, improving your credit score and shopping around can help you secure a better deal.

Tips to Manage Your APR

- Build and protect your credit score. Pay your bills on time, keep credit utilization low, and avoid opening too many accounts.

- Compare offers carefully. Look at both the APR and the APY (if available) to understand the true cost of borrowing or potential earnings.

- Understand fee structures. Ask lenders which fees are included in the APR and which are not. Consider total costs, not just the rate.

- Pay balances in full. With credit cards, avoiding interest entirely is possible when you pay your balance each month. Otherwise, compounding interest and fees can quickly increase your costs.

- Consider fixed rates. In a rising-rate environment, a fixed APR may provide peace of mind and protect you from future rate hikes.

FAQs

Q1. What does APR stand for?

APR stands for annual percentage rate. It shows the yearly cost of borrowing or earnings from an investment, including interest and certain fees.

Q2. How is APR different from an interest rate?

While an interest rate reflects the cost of borrowing money, the APR adds many fees to provide a more comprehensive view of annual costs.

Q3. Why is my credit card APR higher than my mortgage rate?

Credit cards are unsecured loans, so lenders charge higher APRs to compensate for greater risk. Mortgages are secured by your home, allowing lenders to offer lower rates.

Q4. How can I reduce my APR?

Improve your credit, pay down existing debt, and shop around for better offers. Refinancing or transferring balances to a lower-rate card can also help.

Q5. Is a zero-percent APR offer a good deal?

Introductory 0% APRs can save money if you pay off the balance before the promotional period ends. After that, a higher standard APR kicks in, so read the terms carefully.

Summary

Understanding the annual percentage rate (APR) helps you see the true cost of borrowing. It combines interest and certain fees into a single annual percentage, making it easier to compare financial products. However, APR does not include compounding, so the actual cost may be higher. By carefully reviewing APR, improving your credit score, and comparing offers, you can make smarter borrowing decisions and avoid unnecessary costs. Always read the terms to ensure you fully understand what you are paying.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.