Project risk is not just about what might go wrong. It is about how uncertainty shapes every decision you make. Have you ever planned everything well, only for things to change? That is where understanding event risk vs non-event risk becomes essential. These two risk types affect projects in very different ways. Event risks are sudden and visible, like a supplier failure or a storm. Non-event risks are quieter but just as powerful. They come from uncertainty in estimates, assumptions, or knowledge gaps.

So, what is the difference between event risk and non-event risk? Event risk is the possibility that a future event may occur. Non-event risk is uncertainty within a situation that already exists, such as variability or ambiguity.

In today’s blog post, I will explain the event risk, non-event risk and their differences.

Key Takeaways

- Event risks: Happen as discrete events that may or may not occur. They are external to your project and beyond your control (e.g., a hurricane or supplier bankruptcy).

- Non-event risks: Arise from inherent uncertainty in a plan. They include variability (where outcomes vary within a known range) and ambiguity (where information is incomplete).

- Planning strategies: Event risks are handled through a risk register, contingency plans and traditional risk analysis. Non-event risks require tools like Monte Carlo simulation, incremental development, and expert consultation.

- Why it matters: Knowing the risk type improves your ability to allocate resources, set realistic schedules and communicate with stakeholders. It’s also essential for PMP exam preparation.

What is Event Risk?

Event risk refers to a possible future event that could influence your project’s objectives. It might bring opportunity or cause harm, but it remains outside of your direct control. These risks are sometimes called stochastic uncertainties because they involve random factors. Project managers can identify event risks through brainstorming, expert judgment and historical data, but cannot predict whether they will occur.

Event Risk Examples

Consider these situations:

- Severe weather: A hurricane disrupts a construction project, requiring schedule changes and safety measures.

- Supplier failure: A key vendor goes out of business, forcing you to find alternate suppliers and adjust costs.

- Regulatory change: New laws impose restrictions or additional documentation, affecting project scope.

- Client decisions: The client changes requirements after the design is complete, resulting in rework and delays.

Each of these events may or may not happen, but if they do, they can significantly influence cost, time or quality.

Planning for Event Risk

Event risks are documented in a risk register. For each risk, you note the likelihood, impact, triggers and response strategies. Traditional risk analysis techniques, such as qualitative and quantitative assessments, help prioritize which risks deserve contingency reserves. For example, allocating extra time in the schedule or setting aside a budget contingency can mitigate the impact of an event risk. Regular risk reviews ensure that new event risks are captured throughout the project lifecycle.

What is Non-Event Risk?

While event risks are discrete occurrences, non-event risks stem from uncertainty in a project’s parameters. These risks relate to what you don’t know about the variables that define your plan, such as time estimates, cost assumptions or technological feasibility. PMI’s PMBOK Guide notes two forms of non-event risk: variability and ambiguity to help teams better identify and manage them.

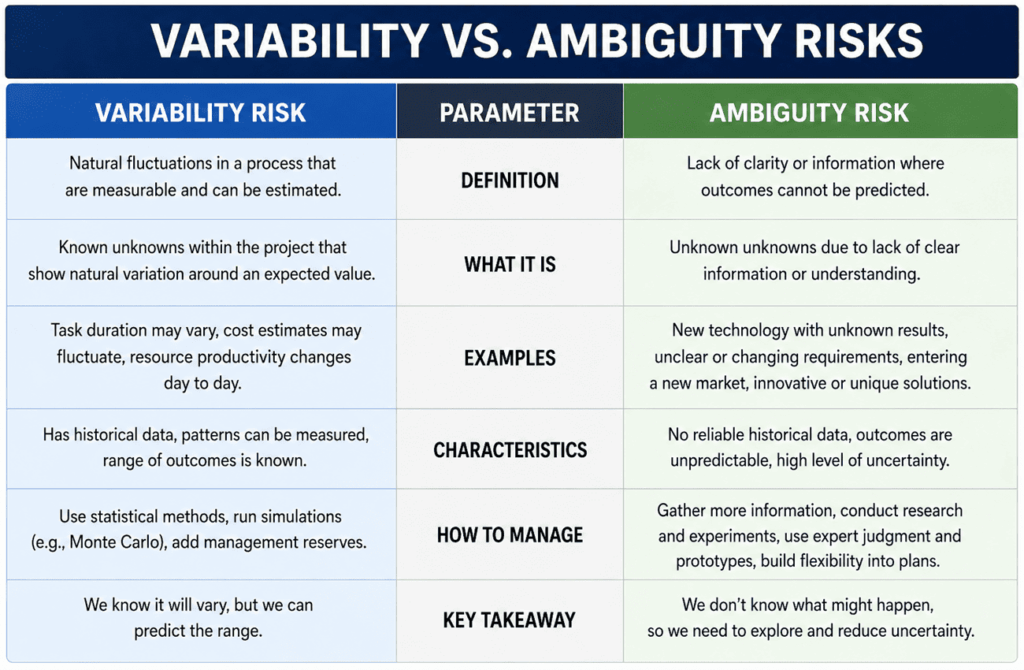

Variability Risk

Variability risks arise when you know the possible outcomes but not which one will occur. They reflect randomness within known limits. For example, productivity may be above or below your target, the number of defects may vary during testing, or unseasonal weather may delay construction. These outcomes are expected; you just don’t know the exact value ahead of time.

Planning tip: Since variability deals with ranges, Monte Carlo simulation helps model different scenarios for cost, time or resource requirements. Using probability distributions gives you a clearer view of the range of outcomes and enables you to set realistic contingency reserves.

Ambiguity Risk

Ambiguity risks occur when you lack sufficient knowledge about a situation. Unclear requirements, emerging technology, uncertain market conditions or evolving regulations fall into this category. Ambiguity is unsettling because you cannot even define the range of outcomes.

Planning tip: Reducing ambiguity requires gathering more information. Techniques such as expert consultation, benchmarking, prototyping and incremental development allow you to learn quickly and adjust. As you convert unknowns into knowns, your risk response becomes more accurate.

Non-Event Risk Examples

- Productivity variation: Team productivity fluctuates because individuals work at different speeds or encounter unforeseen technical challenges.

- Unseasonal weather: Weather that is unusual for the season slows work but is within the expected range.

- Adoption of new technology: Using unfamiliar software or hardware introduces uncertainty because the learning curve and integration issues are unclear.

- Market shifts: Competitor actions or sudden changes in consumer demand affect project priorities.

Event Risk Vs Non-Event Risks

Understanding how event and non-event risks differ helps you choose the right management strategy. Event risks are external and occur as discrete incidents; non-event risks are inherent and relate to the parameters of your plan.

The table below summarizes the differences between event and non-event risks:

| Parameter | Event Risk | Non-Event Risk |

| Definition | A possible future event that may or may not happen | Uncertainty within an existing plan or situation |

| Nature | Discrete and visible | Continuous and subtle |

| Cause | External triggers (e.g., weather, supplier failure) | Internal uncertainty (e.g., estimates, assumptions) |

| Predictability | Can be identified but not predicted exactly | Known uncertainty, but the exact outcome is unclear |

| Examples | Hurricane, regulatory change, resource loss | Productivity variation, unclear requirements, and new technology |

| Impact | Occurs if the event happens | Exists even without a specific event |

| Identification | Listed in a risk register | Found through analysis of variables and knowledge gaps |

| Management Approach | Contingency planning, risk response strategies | Simulation, expert input, prototyping |

| Visibility | Easy to recognize when it occurs | Harder to detect early |

| PMP Exam Focus | Traditional risk management | Advanced risk concepts (variability and ambiguity) |

Why Distinguishing Matters

- Resource allocation: Event risks often need contingency reserves, while non-event risks may require statistical analysis and iterative planning.

- Communication: Explaining whether a risk is external or inherent helps stakeholders understand why certain decisions are made. For instance, telling sponsors that a natural disaster is an event risk emphasizes the need for contingency, whereas an ambiguous requirement suggests the need for further analysis.

- Exam preparation: The PMP exam tests your ability to classify risks correctly. Being able to distinguish between event and non-event risks, and between variability and ambiguity, can earn valuable points.

Planning for Non-Event Risks

Effective non-event risk planning requires a combination of statistical tools and adaptive practices:

- Use probability distributions: For variability risks, apply techniques such as Monte Carlo simulation to estimate ranges for cost and schedule.

- Gather expert input: Bring in specialists to clarify ambiguous requirements or provide insights into emerging technologies.

- Prototype and iterate: Develop small, incremental versions of deliverables to test assumptions and reduce ambiguity.

- Benchmark: Compare your project to similar efforts to gauge typical ranges for key metrics. Real-world data helps narrow uncertainty.

The following infographic summarises the risks of variability and ambiguity.

Event Vs Non-Event Risk for PMP Exam Candidates

If you’re studying for the PMP exam, expect questions that ask you to classify risks and choose appropriate responses. Here are some study tips:

- Know the definitions: Ensure you can distinguish event risk from non-event risk and identify the difference between variability and ambiguity.

- Understand risk processes: Review how risks are identified, analyzed, and monitored.

- Practice with sample questions: Test your understanding. Practice helps you recognize how questions are framed and reduces exam anxiety.

- Stay current: Keep up with industry reports, such as the Allianz Risk Barometer and PMI’s Pulse of the Profession, to understand emerging risks. New exam questions may reflect recent trends.

FAQs

Q1. What’s the difference between event risk and non-event risk?

Event risk is a discrete occurrence, such as a storm or a supplier failure. Non-event risk arises from inherent uncertainty, such as varying productivity or ambiguous requirements.

Q2. How can project managers plan for variability risk?

They can model ranges using probability distributions and Monte Carlo simulation, then adjust the schedule and cost reserves accordingly.

Q3. What tools help reduce ambiguity risk?

Expert consultations, prototyping and benchmarking provide more data and shrink the unknowns, making planning more accurate.

Summary

Understanding event risk vs non-event risk helps you manage uncertainty with confidence. Event risks are visible and easier to track, while non-event risks hide within assumptions and estimates. Both can affect your project if ignored. By identifying each type early and applying the right tools, you improve planning and decision-making. This knowledge also strengthens your PMP exam readiness. In the end, better risk awareness leads to stronger, more resilient projects that can handle change effectively.

This topic is important for the PMP exam.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.