Understanding the difference between interest rate vs APR is essential when choosing a mortgage or any loan. These two terms may look similar, but they represent different costs of borrowing. The interest rate shows the basic cost of the loan, while the APR provides a broader view by including fees and additional charges. Many borrowers focus only on the interest rate and overlook the APR, which can lead to higher overall costs.

By learning how APR Vs interest rate works, you can compare loan offers more accurately and make smarter financial decisions.

In this blog post, I will explain annual percentage rate, interest rate, and their differences in simple terms so you can choose the most cost-effective mortgage with confidence.

Key Takeaway

- Interest rate: The price you pay the lender for the loan principal. It doesn’t include extra fees.

- APR: A broader measure of loan cost that includes interest plus fees, points, and mortgage insurance. It’s usually higher than the interest rate.

- Comparison tip: Always compare APRs when shopping for mortgages because fees vary by lender. Your monthly payment is based on the interest rate, but the APR reflects the total cost over time.

What is an Interest Rate?

An interest rate is the cost you pay to borrow money from a lender. It’s expressed as a percentage of your principal balance. For mortgages, the interest rate determines how much interest you’ll owe on top of the amount you borrow, and it directly influences your monthly payment. According to the Consumer Financial Protection Bureau (CFPB), the interest rate is the cost you pay for borrowing, in addition to your loan amount. A higher rate means you’ll pay more over the life of the loan.

Several factors influence your interest rate:

- Credit score and debt-to-income ratio. Borrowers with higher credit scores and lower debt tend to receive lower interest rates because they pose less risk to lenders.

- Loan term and type. Fixed-rate loans, adjustable-rate loans, and government-backed loans all have different rate structures. Shorter terms usually offer lower rates.

- Market conditions. Mortgage rates move with broader economic factors. As of April 2 2026, the average 30-year mortgage rate was 6.25 percent, and the average 15-year rate was 5.75 percent.

What is APR?

APR stands for annual percentage rate. It represents the total cost of borrowing and includes both the interest rate and lender fees such as origination charges, discount points, and mortgage insurance. The CFPB notes that the APR is the interest rate plus any additional fees charged by the lender. Because it incorporates fees, the APR is almost always higher than the quoted interest rate.

Why regulators require APR disclosure

The federal Truth in Lending Act (TILA) requires lenders to provide you with a clear disclosure of your APR before you sign your loan documents. This regulation was designed to help consumers accurately compare loans. Since lenders must calculate APRs using the same rules, you can compare two mortgage offers by their APRs even if their fee structures differ.

What’s included in APR?

APR adds common mortgage costs to the interest rate:

- Origination and application fees. Lenders may charge fees to process your loan.

- Discount points. You may pay points up front to lower your interest rate. Those costs are included in your APR.

- Mortgage insurance and other charges. Some loans require mortgage insurance or government fees. These costs are included when calculating the APR.

APR does not determine your monthly payment; your payment is based on the interest rate and loan term. The APR simply converts fees into an annual percentage to show the true cost of financing. For most mortgages, closing costs can range from 2 percent to 5 percent of the loan amount, which is why APRs are often noticeably higher than interest rates.

Interest Rate Vs APR: Main Differences

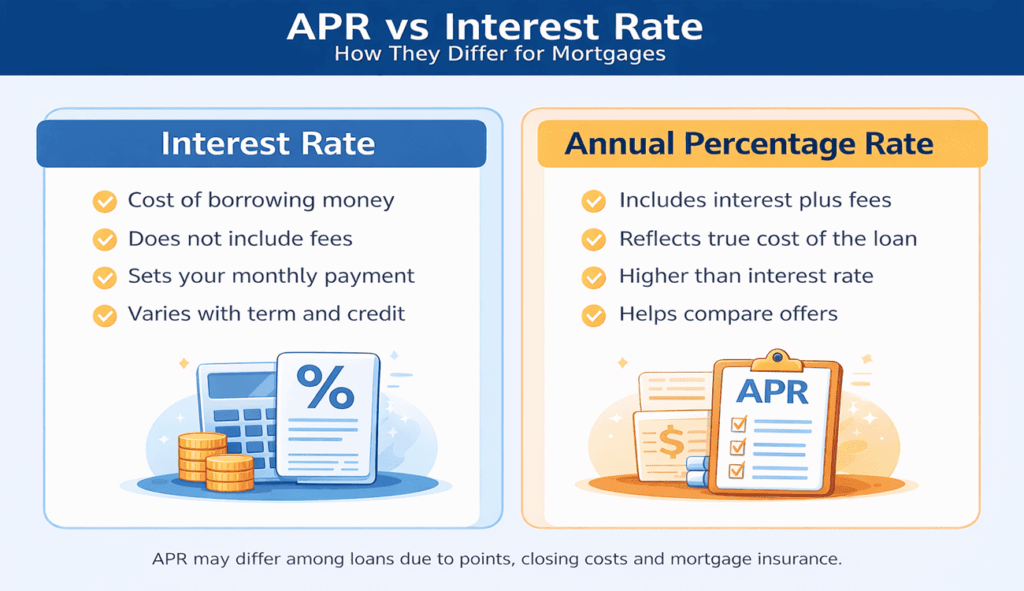

The key difference between the interest rate and the APR is that the interest rate covers only the cost of borrowing money, while the APR includes the interest and most fees. The APR provides a more comprehensive picture of what you’ll pay over the life of the loan. The infographic below summarizes these differences.

The left side shows that the interest rate determines your monthly payment and doesn’t include fees. The right side highlights that APR includes lender fees, making it a more holistic measure. Because APR accounts for costs, it allows you to compare offers from different lenders even when some fees are rolled into the rate, and others are charged upfront.

Why APR Matters for Borrowers

APR is more than just another number on your Loan Estimate; it’s a tool for smart comparison. Since TILA requires lenders to calculate APR in the same way, you can evaluate loans with different fee structures side by side. For instance, one lender might advertise a low rate but charge high origination fees. Another lender might offer a slightly higher rate but waive most fees. Looking only at the interest rate might lead you to choose the first loan, yet its APR could be higher once fees are considered.

In addition, APR helps you gauge the impact of buying discount points. Paying points can lower your interest rate and monthly payment, but it increases your upfront costs. The APR shows whether the long-term savings from a lower rate outweigh the upfront expenditure.

Remember that your monthly payment is calculated using the interest rate, not the APR. So while APR helps compare loans, you still need to budget based on the interest rate and loan term. If you plan to stay in your home for only a few years, a loan with a lower rate and higher fees might not be worth it because you won’t have enough time to recoup the upfront costs through interest savings.

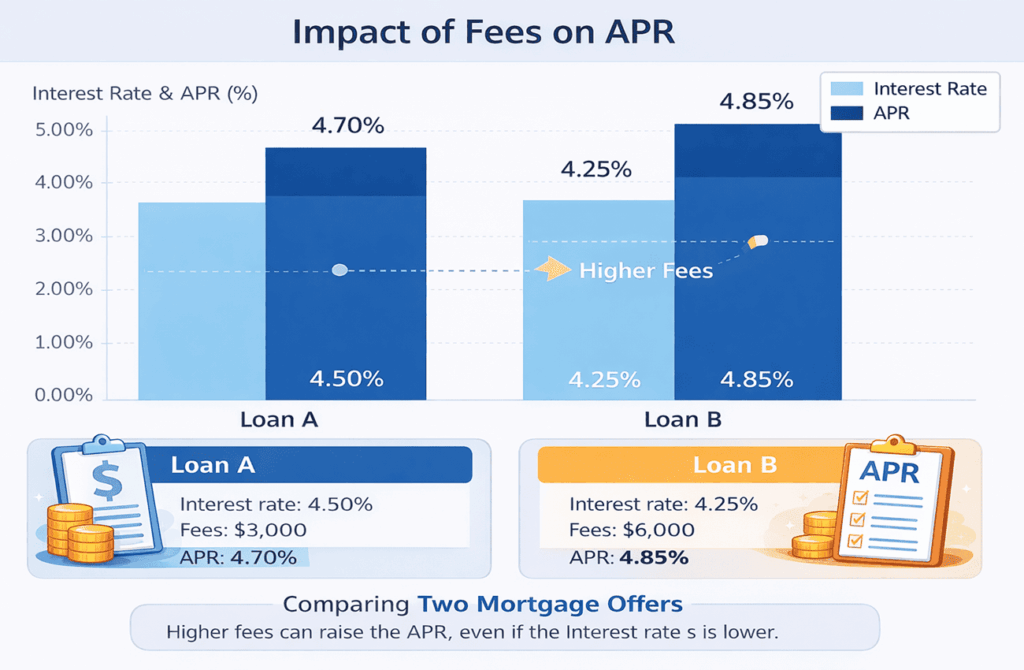

Example: Comparing Two Mortgage Offers

Suppose you have two mortgage offers for a 30-year loan of $300,000. Loan A has a 4.5 percent interest rate with $3,000 in fees. Loan B offers a 4.25 percent interest rate but charges $6,000 in fees. Intuitively, Loan B’s lower rate seems attractive. However, when fees are rolled into the cost of borrowing, the APR tells a different story. The infographic below illustrates how the APR changes.

In this example, Loan A’s interest rate of 4.5 percent yields an APR of 4.7 percent after accounting for its $3,000 in fees. Loan B’s interest rate is lower at 4.25 percent, but because the fees are higher, its APR rises to 4.8 percent. If you keep your mortgage for the full term, Loan A may be cheaper overall despite the slightly higher rate. This example shows why you should always compare APRs rather than interest rates alone.

Tips to Get the Best Rate and APR

- Strengthen your credit profile. Pay down existing debt, make payments on time, and check your credit report for errors. Lenders reward borrowers with good credit by offering lower rates and fees.

- Shop around. Request Loan Estimates from at least three lenders. Because fees vary widely, comparing APRs can save thousands over the life of your loan.

- Consider points carefully. Buying discount points can reduce your rate, but you need to stay in the home long enough to break even. Ask your lender to calculate the breakeven point.

- Increase your down payment. A bigger down payment lowers the amount you need to borrow, which may qualify you for a lower rate and reduce your APR.

- Ask about fee waivers. Some lenders may waive or reduce origination fees, especially if you have a strong banking relationship.

FAQs

Q1. Why is my APR higher than my interest rate?

Your APR includes lender fees, such as origination, discount points, and mortgage insurance, along with the interest rate. Because it bundles these costs, your APR is usually higher than your interest rate.

Q2. Does a lower interest rate always mean a cheaper loan?

Not necessarily. A lender could offer a low rate but charge high fees. Compare the APRs of different offers to see which loan is cheaper over time.

Q3. How can I lower my APR?

Improve your credit, negotiate fees, and shop around for better terms. Paying a larger down payment or avoiding unnecessary points can also reduce your APR.

Q4. Should I focus on APR or interest rate?

Look at both. Use the interest rate to estimate your monthly payment and the APR to compare the total cost of different loans. Together, they give a full picture of affordability.

Summary

Understanding interest rate vs APR helps you make smarter borrowing decisions. While the interest rate determines your monthly payment, the APR reveals the true cost of the loan by including fees. Comparing both ensures you don’t overlook hidden costs. Always review loan offers carefully, consider your long-term plans, and shop around for the best deal. By focusing on both APR and interest rate, you can choose a mortgage that is affordable today and cost-effective over time.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.