Saving money should do more than keep funds safe. It should help those funds grow.

The annual percentage yield (APY) shows how much your money can earn in a year when interest compounds.

Unlike a simple interest rate, APY accounts for the effect of interest piling onto interest. Because of that, APY offers a clearer picture of potential growth on savings accounts, certificates of deposit, and other interest-bearing products. This post explains APY in plain terms and shows how you can use it to make smart saving decisions.

Key Takeaway

- APY shows the actual growth of your money. It accounts for compounding, so even a small difference in APY can lead to noticeable gains over time.

- The formula for APY depends on the nominal rate and the compounding frequency. APY increases when interest is compounded more frequently.

- High-yield accounts usually offer APYs several times higher than the national average. The average savings yield in April 2026 was 0.6% APY. Many online banks offered APYs of around 4% or more.

- Central bank policy influences APY. When the Federal Reserve changes its benchmark rate, banks adjust what they pay on deposits.

- Comparing APY to APR helps you understand the difference between earning and borrowing. APY measures what you earn on deposits, while the annual percentage rate (APR) shows what you pay on loans.

Understanding Annual Percentage Yield

APY stands for annual percentage yield. It measures the percentage gain on a deposit over one year, including the compounding of interest. When money earns interest, that interest is added to the balance. In the next period, you earn interest on the new, larger balance. That cycle is called compounding. The more often interest compounds, the faster your balance grows.

To see how compounding makes a difference, imagine depositing $1,000 in a savings account with a 5% nominal rate. If interest compounds only once at the end of the year, you’ll earn $50 and end up with $1,050. If it compounds monthly, each month’s interest is added to the balance, so by the end of the year, you’ll have a bit more than $1,050. Over time, this small difference grows bigger.

APY helps you compare accounts with different compounding schedules. For example, a money market account with a 6% nominal rate compounded monthly will have a higher APY than a zero-coupon bond that pays 6% once at the end of the year. Because APY standardizes returns, you can fairly evaluate which account offers better growth.

How to Calculate APY

The general formula used by banks to calculate APY looks like this:

Where:

- r is the nominal (stated) annual interest rate.

- n is the number of compounding periods per year (monthly compounding means n = 12).

Regulators also express APY as an annualized rate using a formula that accounts for the total dollar amount of interest earned over a given term. When the deposit term is exactly one year, the simplified formula is APY = Interest / Principal.

This infographic illustrates the relationship between the nominal rate (r), the number of compounding periods (n), and the resulting APY. As n increases, each period’s interest is applied to a slightly larger balance, which boosts the annual yield.

To calculate APY by hand, follow these steps:

- Convert the nominal rate to a decimal (for example, 5% becomes 0.05).

- Divide the nominal rate by the number of compounding periods. For monthly compounding at 5%, that’s 0.05 / 12.

- Add 1 to the result, then raise that value to the power of the number of compounding periods (12 for monthly).

- Subtract 1 from the result. The final number is the APY as a decimal.

- To express APY as a percentage, multiply by 100.

Financial institutions calculate APY automatically, but understanding the formula helps you appreciate how compounding increases earnings. When comparing accounts, look for a higher APY rather than focusing solely on the nominal interest rate.

APY Vs Simple Interest Rate

An interest rate tells you how much you will earn over a period, but it doesn’t account for compounding. APY reflects the true annual growth because it includes interest on interest. Here’s how they differ:

| Metric | What It Represents | Calculation |

| Nominal interest rate | The stated rate on an account does not include compounding | Rate multiplied by principal |

| APY | The annualized return, including compounding | (1 + r/n)^n – 1 |

Because APY captures compounding, it will always be equal to or higher than the nominal rate for positive interest rates. The difference grows as the compounding frequency increases. For example, a 6% nominal rate compounded monthly yields an APY of about 6.17%.

APY Vs APR: Earning Vs Borrowing

APY and annual percentage rate (APR) both express interest as an annual percentage, but they apply to different situations. APY is used for deposits and investments to show how much you earn. It includes the benefit of compounding. APR is used for loans and credit products to show how much you owe. It usually excludes compounding but may include fees.

If you’re evaluating a savings account or CD, focus on APY. If you’re comparing loans or credit cards, look at APR. Keep in mind that some lending products advertise a low rate but charge high fees; a higher APR indicates that borrowing costs are greater than the stated rate suggests. Similarly, an account with a higher APY may still have fees that eat into earnings, so always read the fine print.

Example: How APY Works in Practice

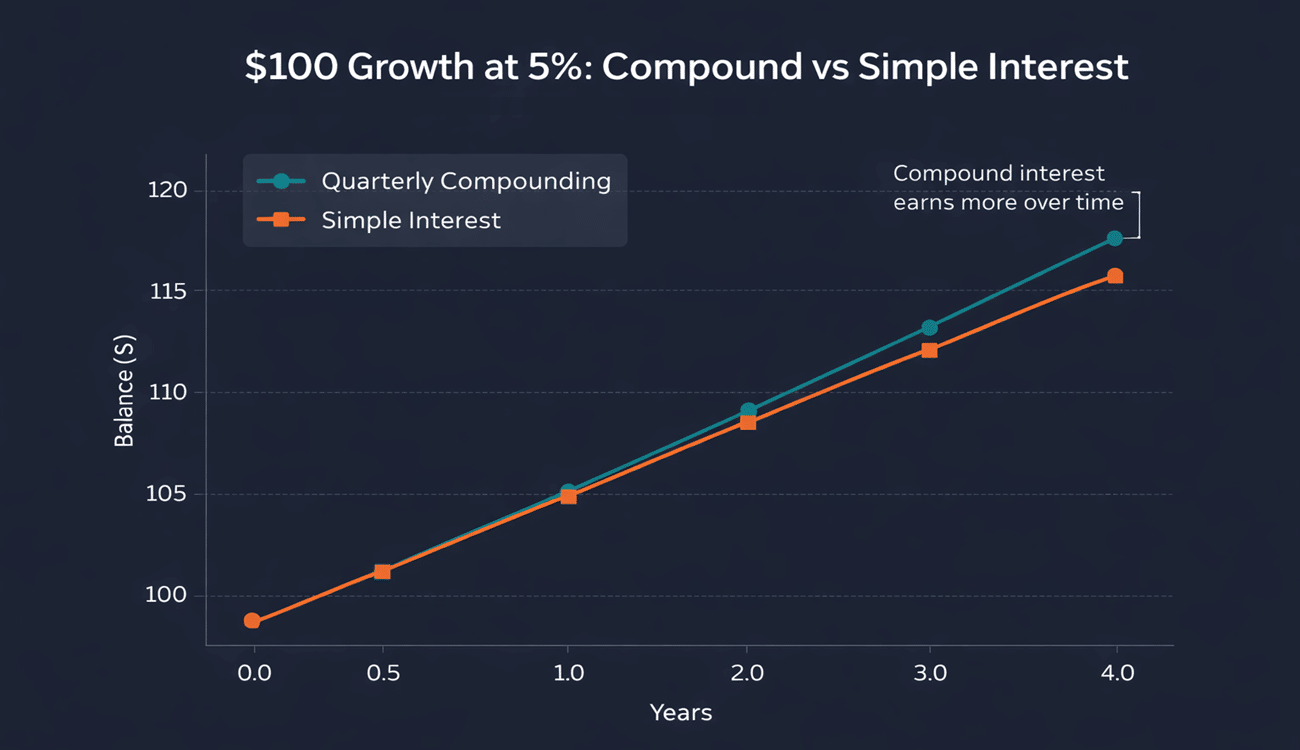

Consider a $100 deposit in an account offering a 5% nominal rate compounded quarterly. At the end of the year, your balance would not be $105. It would be approximately $105.09, because interest is added every quarter and then earns interest in subsequent quarters. The APY for this deposit is about 5.095%[5]. Though the extra nine cents may seem small, compounding becomes more powerful as the balance and time horizon increase.

The chart below compares the growth of $100 over four years with simple interest versus quarterly compounding at 5%. Notice how the compounded balance pulls ahead over time.

Tips to Maximize Your APY

- Compare rates regularly. Banks update APYs as market conditions change. If your current account’s rate falls below those offered elsewhere, moving your savings can improve your earnings.

- Watch the Fed. A change in the federal funds rate is likely to ripple through deposit rates. Pay attention to economic news so you can act before a rate shift reduces your earnings.

- Consider a ladder. If you don’t know when you’ll need your money, splitting funds among accounts with different terms can balance accessibility and return.

- Avoid unnecessary fees. Monthly maintenance fees or minimum balance charges can wipe out the extra yield from a higher APY. Choose accounts with low or no fees.

FAQs

Q1. What does APY stand for?

APY stands for annual percentage yield. It represents the rate of return on a deposit over one year, including interest compounding.

Q2. How is APY different from APR?

APY measures what you earn on savings, while APR measures what you owe on loans. APY includes compounding; APR generally does not and may include fees.

Q3. Does a higher APY always mean a better account?

Not always. A higher APY can be offset by fees or balance requirements. Always read the terms and compare net earnings after any charges.

Q4.How often can banks change variable APYs?

Banks can adjust a variable APY at any time. They often react to changes in the Federal Reserve’s benchmark rate and market competition.

Q5. Is APY affected by inflation?

APY is the rate your bank pays. Inflation erodes the purchasing power of your earnings. A good practice is to choose an APY that stays ahead of the inflation rate.

Summary

Annual percentage yield (APY) is a key measure that reflects the true earning potential of your savings by accounting for compounding. Even small differences in APY can lead to significant gains over time. By understanding how APY works, comparing rates across accounts, and monitoring market trends, you can make smarter financial decisions. Choosing the right account with a competitive APY ensures your money grows efficiently and supports your long-term financial goals.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.