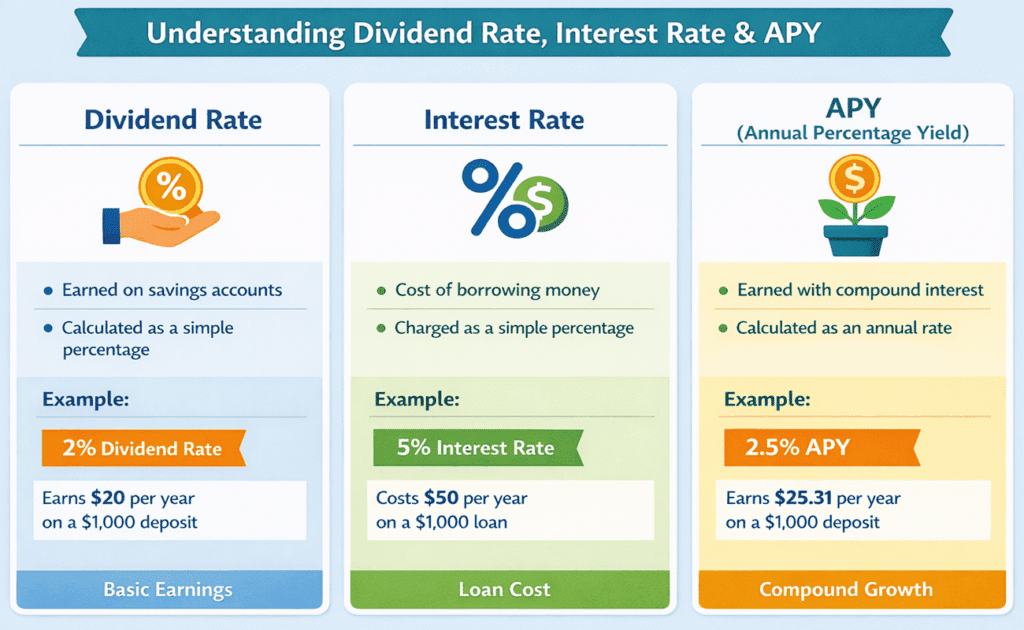

When you compare savings accounts, certificates of deposit (CDs), or money market accounts, you will see two numbers: the dividend rate (also called the interest rate) and the annual percentage yield (APY). At first glance, they might look similar, but they tell different stories about your money.

The dividend rate is the base rate a bank or credit union uses to calculate earnings. APY captures how often those earnings are added to your balance. The distinction matters because it can change how quickly your savings grow.

In this blog post, I will break down the difference between the dividend rate and APY so you can make confident choices.

Key Takeaway

- Dividend or interest rate: The base percentage used to calculate how much you earn or owe. It does not include compounding.

- Annual percentage yield: This figure accounts for compounding and shows what you actually earn over a year. APY is always equal to or higher than the dividend rate for savings accounts.

- Compounding frequency matters: Accounts that compound monthly or daily will have a higher APY than accounts with the same base rate that compound annually. That difference grows over time.

- Use APY for comparisons: When choosing between savings products, compare APYs rather than just the dividend rate. APY reflects the real return on your money.

- National trends: As of April 3, 2026, the national average savings account yield was 0.6% APY, while high-yield online banks offered around 4% APY. Knowing these benchmarks helps you evaluate offers.

Understanding the Dividend Rate

What Is a Dividend Rate?

A dividend rate is the percentage a credit union pays on savings accounts, similar to a bank’s interest rate. Because credit unions are member-owned, they share earnings as dividends rather than profits. The dividend rate shows how much you can earn on your balance over a year, but it does not include compounding.

For example, if your account has a 3% dividend rate, a $1,000 balance earns $30 annually before compounding. While helpful, the dividend rate alone does not reflect total earnings.

How Does an Interest Rate Compare?

In banks and other lenders, the term interest rate is more common. It is the basic rate charged on loans or paid on deposits. If a bank offers a loan at 5% interest, you pay 5% of the outstanding balance each year. For deposits, the interest rate is the starting point for your earnings. Whether the account is labeled as “interest” or “dividend,” the concept is the same: it is the base rate before considering compounding.

Example of a Basic Interest Rate

Imagine a basic savings account with a 3 % interest rate that compounds once per year. If you keep $1,000 in the account, you earn $30 in interest at the end of the year. You could think of this as simple interest: there is no additional growth on the interest itself during the year. Without compounding, the interest rate and APY would be the same.

Annual Percentage Yield

What is APY?

The annual percentage yield (APY) shows the total amount of interest you earn in a year when compounding is taken into account. Under U.S. federal rules, financial institutions must disclose APY to make it easier to compare deposits. APY includes two factors: the interest rate and the frequency of compounding. If an account compounds more often, the APY will be slightly higher because each interest payment starts earning interest of its own.

Why APY Exceeds the Dividend Rate

APY is always equal to or higher than the dividend rate on savings accounts because it reflects this extra boost from compounding. For example, a 1% interest rate compounded monthly yields an APY of about 1.01%, whereas annual compounding yields an APY of exactly 1%. That small difference may seem minor on a $1,000 balance, but over many years and larger balances, it adds up.

How APY Is Calculated

APY can be calculated with this formula:

where r is the annual interest rate, and n is the number of compounding periods in a year. For monthly compounding, n = 12; for daily compounding, n = 365. The more frequently interest is added, the more compounding cycles there are, and the higher the APY.

APY Vs APR

While APY measures what you earn on deposits, annual percentage rate (APR) refers to what you owe when borrowing. APR includes certain fees and expresses the cost of a loan over a year. APY helps you compare savings accounts, money market accounts, and certificates of deposit, whereas APR helps you shop for mortgages, car loans, or credit cards.

The Power of Compounding

How Compounding Works

Compound interest is interest paid on both the principal and the accumulated interest. Compound interest lets you earn interest on the money you’ve saved, and on the interest you earn along the way. In a simple example, if you invest $1,000 at a 5% annual interest rate, you earn $50 in the first year. In the second year, you earn $52.50 because you’re earning 5 % not just on the original $1,000, but also on the $50 earned in the first year.

Compounding Frequency and APY

The frequency of compounding significantly influences APY. An account that compounds daily will add interest 365 times a year, giving each dollar of interest more opportunities to earn. Accounts that compound monthly add interest 12 times a year, still more often than annual compounding.

PNC’s example shows that two accounts with the same 1% interest rate produce different APYs when one compounds monthly and the other annually. Daily compounding yields a higher APY because interest is added more frequently.

Dividend Rate Vs APY: A Head-to-Head Example

Comparing Two Accounts

Let’s compare two fictional credit union savings accounts, both with a 3% dividend rate but different compounding frequencies.

This example illustrates why APY matters.

| Account | Dividend / Interest Rate | Compounding Frequency | Resulting APY |

| Account A | 3.00 % | Annual | 3.00 % |

| Account B | 3.00 % | Monthly | 3.04 % |

Explanation: Account A compounds once per year, so the APY matches the dividend rate. Account B compounds 12 times per year, yielding a slightly higher APY of 3.04% because interest starts earning interest sooner. Over long periods, that difference can meaningfully boost your savings.

Why Small Differences Add Up

The compounding difference shown above may appear small when you’re only looking at one year. However, consider a balance of $10,000. Account A would earn $300 after one year, whereas Account B would earn about $304. Over five years, Account A grows to approximately $11,593, while Account B grows to about $11,628. That extra $35 comes from compounding the interest sooner. When you extend the timeline to ten or twenty years, the gap widens even more.

Longer-Term Impact

Compound interest becomes more powerful over longer periods. At a 4% APY, a $10,000 deposit grows to roughly $14,800 after 10 years without additional contributions. If the APY remains at 4.5%, the same deposit could grow to around $15,550. Each small increase in APY boosts the final balance because interest compounds on every dollar earned along the way. This is why high-yield savings accounts often lead to substantially higher earnings over time.

How to Compare Savings Products Using APY

Look Beyond the Rate

When evaluating savings accounts, money markets, or certificates, always compare APYs rather than just the dividend rate. Financial institutions are required to disclose APYs so that consumers can easily see the real return. Comparing APYs ensures that you’re comparing apples to apples: you know how compounding frequency and other factors affect your earnings.

Consider the National Average

Use the national average savings account APY as a benchmark. If the national average is 0.6% APY, and a high-yield online bank offers 4% APY, the difference is significant. Choosing an account with a higher APY means earning more interest. It’s also helpful to check whether the APY is fixed (remains constant for a set term) or variable (changes as market rates change). Many savings and money market accounts have variable APYs that may fluctuate with economic conditions.

Watch for Minimum Balances and Fees

Some accounts require a minimum balance to earn the advertised APY or may impose fees that reduce your earnings. A higher APY might not be worthwhile if you need to maintain a large balance or pay monthly service charges. Always read the account disclosure to understand these requirements and compare them with the APY.

Evaluate Compounding Frequency

Check how often interest is compounded, daily, monthly, or annually. An account with daily compounding often produces a slightly higher APY than one with monthly compounding, even if the interest rate is the same. Because of this, two accounts with identical dividend rates can have different APYs. When the APY is disclosed, compounding frequency is already factored in, but understanding the frequency can help you anticipate how your balance will grow.

Dividend Rate Vs APY in Different Products

Savings Accounts

Savings accounts are the most common place where you’ll see both a dividend rate and APY. They typically compound interest daily or monthly. High-yield online savings accounts often offer APYs several times higher than the national average. When comparing savings accounts, focus on the APY and compounding frequency, and consider any minimum balance requirements.

Money Market Accounts

Money market accounts usually offer competitive APYs and may come with check-writing privileges. They often have tiered APYs, meaning the APY increases when you maintain higher balances. These accounts may require a higher minimum balance to avoid fees, so look at both the APY and the account terms. Because compounding frequency can vary, the APY helps you compare accounts fairly.

Certificates of Deposit (CDs)

CDs pay a fixed dividend rate for a set term, such as six months or five years. They often compound interest monthly or quarterly. The APY on a CD reflects both the dividend rate and the compounding schedule. Longer-term CDs might offer higher APYs, but your money is locked in until maturity. If you withdraw early, you may lose a portion of your interest. Always compare the APY and check the early withdrawal penalties.

Checking Accounts With Interest

Some checking accounts pay interest or dividends. The APY on these accounts may be tiered or depend on meeting certain requirements, such as making a number of debit card transactions or receiving direct deposits each month. When evaluating these accounts, weigh the APY against any fees and the convenience of meeting the requirements.

Tips for Maximizing Your Savings

- Shop around: Use the national average as a starting point, then look for accounts that pay higher APYs. Don’t assume your primary bank offers the best rates.

- Consider credit unions: They often offer competitive APYs and lower fees because they operate as member-owned cooperatives. Joining a credit union can be a smart way to boost your returns.

- Automate savings: Set up automatic transfers to your savings or money market account to consistently build your balance. The more you save, the more compounding can work in your favor.

- Reinvest dividends or interest: If you receive dividends or interest payments, deposit them back into your account or another high-yield product. This simple step increases your principal, which leads to more interest earnings.

- Pay attention to inflation: Inflation reduces the purchasing power of your savings. When inflation is high, a low APY may not keep up. Try to find accounts with APYs that exceed the inflation rate or at least reduce its impact.

FAQs

Q1. How often are dividends compounded?

Dividends on savings, money market accounts, and certificates are commonly compounded monthly or daily. The account disclosure will specify the frequency. More frequent compounding increases the APY.

Q2. Why is the APY higher than the dividend rate on a certificate?

APY reflects compounding. When interest is added to your balance throughout the year and begins earning interest itself, the total annual return, the APY becomes slightly higher than the base dividend rate.

Q3. What is the difference between APY and APR?

APY shows how much you earn on deposits over a year, including compounding. APR is the cost of borrowing, including fees. Use APY for savings accounts and APR for loans.

Q4. Does compounding frequency really make a difference?

Yes. The more often interest is compounded, the more opportunities your earnings have to grow. Over time, even small differences in compounding frequency can lead to higher balances.

Q5. When comparing accounts, should I look at the dividend rate or APY?

Always compare APY. It provides the true annual return because it accounts for both the interest rate and compounding frequency.

Summary

Understanding the difference between the dividend rate and APY empowers you to make smarter saving decisions. The dividend rate is just the starting point; APY reflects the real return by accounting for compounding. By comparing APYs, considering compounding frequency, and shopping around for the best rates, you can maximize your savings over time. If you’re ready to put these principles into action, take the next step with a financial partner that puts members first.

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.