Measuring the value of a project can feel tricky. As a project manager, you need to decide how to invest limited resources. Should you focus on the Net Present Value (NPV) of future cash flows or the Return on Investment (ROI) you expect?

This blog post will break down NPV and ROI metrics, explain their pros and cons, and show how to choose the right one for your project.

Let’s get started.

What Are NPV and ROI?

Net Present Value (NPV) is the value today of a stream of future payments. Because money today is worth more than money tomorrow, cash flows must be discounted at an interest rate. NPV tells you whether discounted inflows exceed the initial investment. It is used in capital budgeting to measure the absolute dollar value of an investment.

For example, discounting $108 received in a year at 8 percent yields $100. If the sum of discounted inflows minus the initial cost is positive, the project adds value.

Return on Investment (ROI) expresses an investment’s efficiency as a percentage. It is the net benefit divided by the initial cost. Unlike NPV, ROI does not consider the timing of cash flows; it simply shows how much the project earned relative to what you spent. ROI is useful for comparing different projects or opportunities. NPV provides a dollar measure, while ROI expresses efficiency; ROI is often preferred when comparing projects.

How to Calculate ROI

Calculating ROI is straightforward. Subtract the project’s total cost from the total value returned and divide by the cost. Then multiply by 100 to get a percentage. For example, if a project costs $10,000 and returns $12,500 at the end of three years, the net gain is $2,500. Dividing $2,500 by $10,000 yields an ROI of 25 percent. ROI can be negative if returns are less than the investment.

How to Calculate NPV

NPV requires discounting future cash flows to the present. Choose a discount rate that reflects your cost of capital or the return you could earn elsewhere. For each future cash flow, divide the amount by (1 + r)^t, where r is the discount rate, and t is the year number. Sum the discounted cash flows and subtract the initial cost. If the result is positive, the project creates value. If it is negative, the project destroys value.

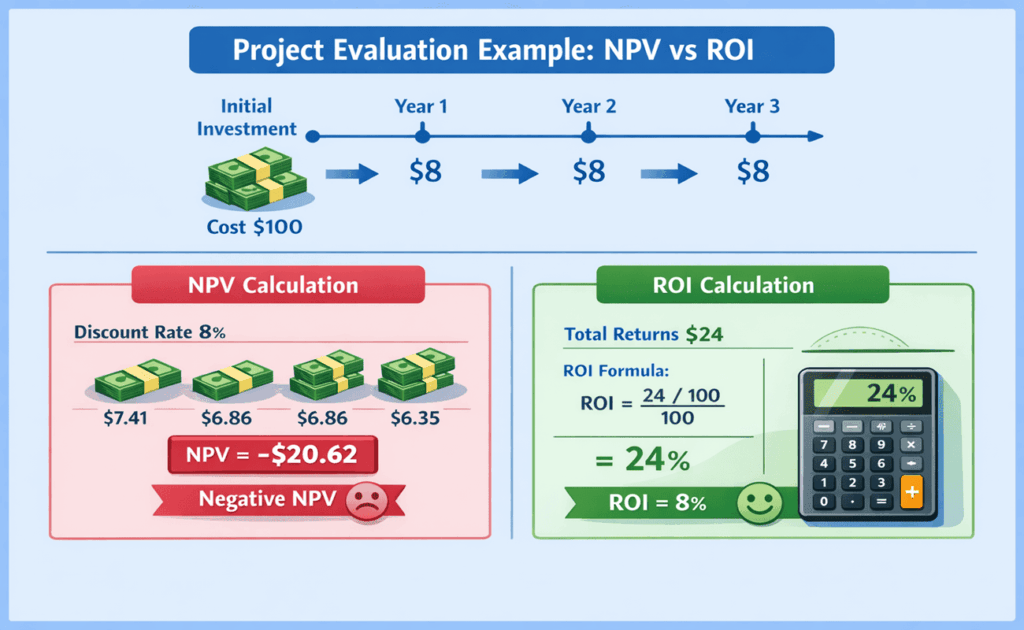

Suppose you invest $100 and expect an annual return of $8 for three years. At an 8 percent discount rate, the present value of the $8 received in Year 1 is about $7.41. Without a residual value, the sum of discounted inflows does not cover the $100 cost, resulting in a negative NPV. The example infographic below illustrates this calculation.

Strengths and Limitations of NPV

NPV helps normalize cash flows to a single point in time. It captures the time value of money and is essential when evaluating long-term capital investments. However, NPV is not a comparison metric. Without an accurate estimate of residual value, the NPV of a technology project will always be artificially low. Moreover, NPV results are highly sensitive to the discount rate and do not indicate the size of the investment. For these reasons, NPV should not be the sole metric for assessing project viability.

Strengths and Limitations of ROI

ROI is easy to compute and communicates results quickly. Because it is a percentage, it allows you to rank projects of different sizes and compare them to your cost of capital. ROI is the primary metric used for evaluating technology investments. Yet ROI ignores the timing of cash flows and can be misleading for long projects. An ROI of 15 percent achieved after five years may be less attractive than a 10 percent ROI realized in one year. ROI also assumes that interim cash flows are reinvested at the same rate, which may not hold in practice.

Why NPV Can Be Negative While ROI is Positive

Nucleus Research identifies three situations where NPV may be negative even if ROI is positive:

- Missing residual value – When no salvage or resale value is included, discounted cash flows may be less than the initial cost, producing a negative NPV.

- Low ROI relative to cost of capital – If the project’s ROI is lower than the organization’s cost of capital, NPV will be negative. A project with a 5 percent return is not viable if your cost of funds is 8 percent.

- Late benefits skew the average – For technology projects, benefits may accumulate in later years. Averaging returns over three years can show a positive ROI, yet discounting those late benefits reduces their present value. Thus, the ROI suggests success while the NPV remains negative.

Project Example: Evaluating a Technology Investment

Consider a project that requires an initial investment of 100 units. It returns 8 units at the end of each of the next three years. The effective ROI is the net gain (24 – 100) divided by 100, or 8%. However, discounting each 8 unit return at an 8 percent cost of capital yields present values of approximately 7.41, 6.86, and 6.35.

The sum of discounted cash flows (about 20.62) is well below 100. With no residual value, the NPV is negative even though the ROI is positive.

This example demonstrates why project managers should compare ROI to the cost of capital and not rely on NPV when residual values are uncertain.

Choosing the Right Metric for Your Project

So which metric should you use? The answer depends on your decision context:

- Capital budgeting and absolute value – Use NPV when evaluating long-term assets or projects with well-defined residual values. NPV indicates whether discounted cash inflows exceed costs and helps maximize shareholder value.

- Comparing multiple projects – Use ROI when ranking projects or when the budget is tight. A higher ROI indicates that each dollar invested yields more benefit. Always compare the project’s ROI with your cost of capital to ensure it adds value.

- Hybrid approach – Calculate both metrics. If ROI exceeds your hurdle rate but NPV is negative, revisit assumptions about residual value or cash flow timing. Sensitivity analysis can reveal how changes in discount rate or expected returns affect NPV.

In practice, ROI is the more versatile measure for project managers. It provides a quick gauge of efficiency, aligns with executives’ thinking, and is widely used across industries. NPV is valuable for large capital projects, but it can mislead when residual values are difficult to estimate or when benefits accrue late.

Practical Tips for Using ROI and NPV

- Set a hurdle rate – Establish the minimum acceptable ROI based on your organization’s cost of capital. Projects with an ROI below this rate should be rejected or redesigned.

- Estimate cash flows realistically – Overly optimistic forecasts will inflate ROI and NPV. Include best-case, base-case, and worst-case scenarios to capture uncertainty.

- Consider qualitative factors – ROI and NPV ignore strategic benefits such as improved customer satisfaction or regulatory compliance. These should be considered alongside financial metrics.

- Review regularly – Recalculate ROI and NPV as projects progress. Actual cash flows may differ from estimates. Adjusting expectations early helps manage risk.

FAQs

Q1. What is the key difference between NPV and ROI?

NPV measures the absolute dollar value created by discounting future cash flows; ROI measures the percentage return relative to cost.

Q2. Can ROI be positive while NPV is negative?

Yes. NPV may be negative if residual value is missing or if ROI is below the cost of capital, even when the average ROI appears positive.

Q3. How should I choose the discount rate for NPV?

Use your organization’s cost of capital or the return you could earn on a similar investment. Higher discount rates reduce NPV and reflect greater risk.

Q4. Is ROI sufficient for project approval?

ROI is a useful screening tool, but it should be compared to the hurdle rate and supplemented with qualitative considerations. For large capital projects, NPV or IRR may also be needed.

Q5. What if my project has uneven cash flows?

In such cases, calculate both ROI and NPV. ROI averages returns, but late cash inflows will have less present value.

Summary

Selecting the right metric depends on your project’s goals and constraints. ROI is simple and powerful for comparing projects and remains the primary tool for evaluating technology investments. NPV is valuable for capital budgeting, but it can mislead when residual values are uncertain or benefits are delayed. By understanding both metrics and their limitations, you can make more informed decisions.

Further Reading:

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.