Every project manager faces tough choices when deciding where to invest limited resources. Should you green-light a new product line or expand an existing facility? The answer often hinges on comparing the cash you expect to receive with the money you need to spend today. That is where net present value (NPV) and internal rate of return (IRR) come in. Both methods discount future cash flow, but they answer different questions.

This blog post explains how NPV and IRR work, when to use one over the other, and how to avoid common traps.

Let’s get started.

What Are Net Present Value and Internal Rate of Return?

Net Present Value Defined

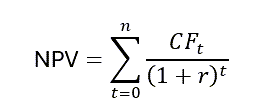

Net present value (NPV) is the sum of all future cash inflows and outflows converted into today’s dollars using a discount rate. It is an absolute value that compares the present value of cash inflows with that of cash outflows.

When NPV is greater than zero, the project’s inflows exceed its costs, signalling that the investment is financially sound. A negative NPV suggests that the project destroys value and should not be pursued.

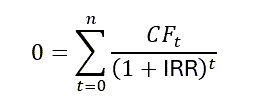

In formula form:

where CFt represents the cash flow in period t and r is the discount rate reflecting the cost of capital or required rate of return.

Internal Rate of Return Defined

The internal rate of return (IRR) is the discount rate that makes the NPV of an investment exactly zero. In other words, it is the break-even rate at which the present value of future cash inflows equals the initial outlay. IRR expresses a project’s profitability as a percentage. When the IRR exceeds the required rate of return, the project is considered acceptable. If the IRR falls below the hurdle rate, the project should be rejected.

Mathematically, IRR solves for r in the NPV equation when NPV = 0:

Unlike NPV, IRR is a relative measure and does not account for project size. This makes it useful for comparing the efficiency of several projects, but it can be misleading for absolute decision-making.

How to Calculate NPV and IRR

The easiest way to compute both metrics is by using spreadsheets or financial calculators. However, manually calculating the result will help you validate the software output.

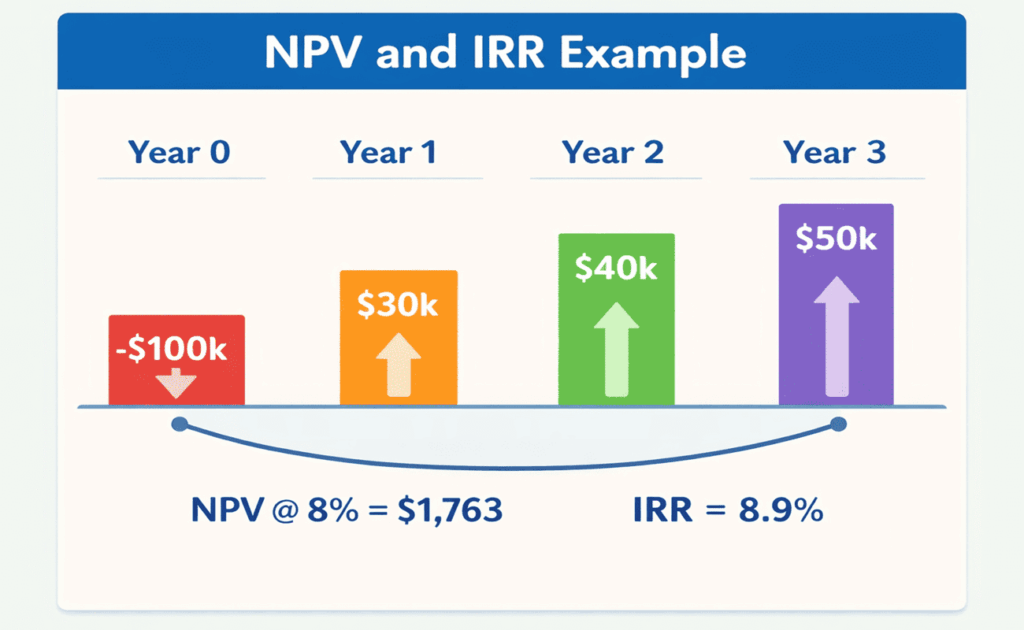

The steps below use a hypothetical project: an initial outlay of $100,000 today (Year 0) followed by cash inflows of $30,000 in Year 1, $40,000 in Year 2, and $50,000 in Year 3. Assume a discount rate of 8%.

- List cash flows by period. Year 0 = –100,000; Year 1 = 30,000; Year 2 = 40,000; Year 3 = 50,000.

- Discount each future cash flow. Divide each inflow by (1 + 0.08)^t. For example, the Year 1 inflow becomes 30,000 / 1.08^1 = 27,778.

- Sum the present values. Add the discounted inflows and subtract the initial cost. In this example, the NPV is approximately $1,763.

- Solve for IRR. Use a numerical method (or the IRR function in Excel) to find the rate that makes NPV = 0. For the same cash flows, the IRR is 8.9%.

The infographic below visualises this example.

Pros and Cons of NPV and IRR

Comparing the benefits and drawbacks of each method helps determine which metric fits your project.

Advantages of NPV

- Time value of money: NPV captures the fact that a dollar today is worth more than a dollar tomorrow.

- Absolute value: It expresses profitability in dollars, making it easy to judge whether a project adds or destroys wealth.

- Risk incorporation: By adjusting the discount rate, you can reflect varying risk levels; recent studies show that risk is captured in the discount rate.

Disadvantages of NPV

- Sensitive to discount rate: Small changes in the hurdle rate can lead to large swings in NPV.

- Requires accurate forecasts: Errors in estimating future cash flows or the cost of capital will distort the NPV.

- Less intuitive for comparing projects: Because it is an absolute dollar figure, NPV does not convey return relative to the investment size.

Advantages of IRR

- Percentage measure: IRR expresses return as a rate, making it easier to compare projects of different scales.

- Simple decision rule: Accept the project when the IRR exceeds the hurdle rate; otherwise, reject it.

- Useful for ranking: When evaluating mutually exclusive projects with similar scale and timing, IRR can help prioritise options.

Disadvantages of IRR

- Multiple IRRs: Projects with alternating positive and negative cash flows may yield multiple IRRs, which can cause confusion.

- Assumes reinvestment at IRR: IRR assumes interim cash flows can be reinvested at the same rate, which is often unrealistic.

- Ignores project scale: A small project with a high IRR might contribute less total value than a large project with a lower IRR.

The following infographic summarises these pros and cons visually.

When Should Project Managers Use NPV or IRR?

Choosing between NPV and IRR depends on the question you are trying to answer.

- Absolute profitability: Use NPV when you need to know whether a project will create or destroy value for the organisation. Because NPV provides a dollar amount, it aligns with the goal of maximising shareholder wealth.

- Ranking similar projects: Use IRR when comparing several projects of similar scale and timing. IRR indicates which option yields the highest return per dollar invested. If two projects have different sizes, compare both NPV and IRR to ensure you do not overlook the larger but slightly lower-return opportunity.

- Uneven cash flows or unknown discount rate: When cash flows change signs multiple times, or the discount rate is uncertain, NPV is more reliable than IRR. IRR can produce multiple values or be undefined in these cases. Modified IRR (MIRR) in Excel can help by assuming reinvestment at the cost of capital rather than at the IRR.

- Regulatory uncertainty: New reporting standards, such as IFRS S1 and S2, introduce sustainability disclosures and increase uncertainty. Research published in 2025 suggests that real-options valuation may capture flexibility better than static NPV. While project managers should still compute NPV and IRR, they should also consider whether deferring or scaling a project adds value when future conditions are uncertain.

Pitfalls and How to Avoid Them

You should be aware of several common mistakes when using NPV and IRR:

- Over-optimistic forecasts. It is tempting to overestimate future cash inflows and underestimate costs. Use conservative assumptions and build scenarios (best-case, base-case, worst-case) to test resilience.

- Ignoring risk adjustments. Do not use the same discount rate across all projects. Riskier projects require higher discount rates to compensate investors. Conversely, lower-risk investments may use a lower cost of capital.

- Misinterpreting multiple IRRs. If your project exhibits alternating cash flow patterns (e.g., outflow, inflow, additional outflow), IRR may return multiple solutions. In such cases, rely on NPV or compute the modified IRR (MIRR), which assumes reinvestment at the cost of capital.

Real-World Application: Assessing a Solar Farm Expansion

Imagine you manage a renewable energy firm considering an expansion of an existing solar farm. The project requires an initial investment of $5 million and is expected to generate $1.5 million in net cash inflows each year for five years. The firm’s cost of capital is 7%.

- Compute NPV. Discount each $1.5 million inflow at 7%, then sum the discounted cash flows. The present value of the inflows is about $6.1 million. Subtracting the $5 million cost yields an NPV of $1.1 million. This indicates that the expansion adds value.

- Find the IRR. Using a spreadsheet, solve for the discount rate that makes NPV = 0. The IRR in this case is roughly 13%. Since the IRR exceeds the 7% hurdle rate, the project is financially attractive.

- Consider non-financial factors. In addition to the numbers, factor in regulatory incentives, environmental impact, and potential maintenance costs. A sensitivity analysis can show how changes in power prices or operating costs affect NPV and IRR.

FAQs

Q1. Can a project have more than one internal rate of return?

Yes. Projects with multiple sign changes in cash flows may have several IRRs or none at all. When that happens, rely on NPV or use modified IRR.

Q2. Why is the NPV greater than zero important?

A positive NPV means the project generates more value than it costs, indicating that it should increase shareholder wealth.

Q3. Is IRR better than NPV for small projects?

It depends. IRR helps compare the efficiency of small projects, but always look at NPV to ensure the total value created meets your organisation’s goals.

Summary

Net present value and internal rate of return help you choose the right investments, but they answer different questions. NPV shows how much value a project adds in today’s money, while IRR shows the expected percentage return. Used together, they balance scale, risk, and timing of cash flows. By linking these metrics to cost of capital and project risk, you can approve projects that truly support strategy, deliver value, and use limited resources wisely across complex global project portfolios.

Further Reading:

- Internal Rate of Return (IRR): Simple Guide & PMP Tips

- Return on Investment in Project Management: Formula, Examples & PMP Exam Tips

- Net Present Value (NPV): Formula, Steps & Examples

- Discounted Payback Period: Definition, Formula & Examples

- Payback Period in Project Management: Definition, Formula, Examples, Pros & Cons

- IRR Vs ROI

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.