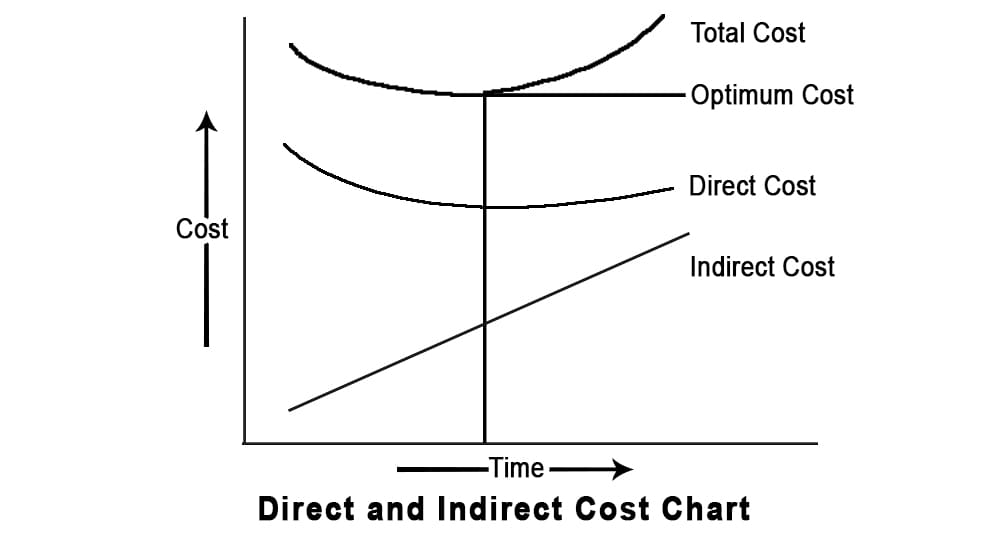

To price your products or services competitively, it is important to understand the difference between direct and indirect costs. Direct costs are those expenses directly tied to producing or delivering a product (e.g., materials or labor). Indirect costs support the production process but aren’t directly linked (e.g., rent or utilities).

Knowing these helps you transparently set prices, calculate profit margins, and communicate financial details with stakeholders. Properly tracking these costs also aids in filing taxes accurately and gets you to benefit from legal concessions, contributing to a clear and sustainable financial strategy.

What Are Direct Costs?

Direct costs are expenses directly linked to producing a product, providing a service, or performing a process. This means they are easily identified as part of the specific activity, like the cost of materials or labor used in production.

By closely tracking direct costs, you can manage the price of your product and make accurate tax calculations.

Controlling direct costs is crucial for managing the overall budget and ensuring the project stays within financial limits.

Direct costs can change frequently due to shifting market conditions, like price fluctuations in materials or labor rates. On an income statement, these costs are recorded under the “Cost of Goods Sold” (COGS) section.

Examples of Direct Costs

Examples of direct costs include:

- Labor: This is wages paid to workers directly involved in production or service delivery.

- Raw Materials: These are materials used to create the product (e.g., wood for furniture or fabric for clothing).

- Consumables: These are supplies that are quickly used up during production (e.g., screws, bolts, or adhesives).

- Staff Salaries: These are salaries of employees who work directly on a project or product (e.g., engineers or assembly line workers).

- Fuel: This includes fuel costs for machinery or transportation directly tied to the project or production.

- Other Direct Expenses: These are costs like packaging for finished products or machinery maintenance specifically for production needs.

All resources directly spent on a project or producing specific goods fall under “direct costs.”

What Are Indirect Costs?

Indirect costs are necessary for maintaining business operations but are not directly linked to producing a specific product or completing a project. These costs cover expenses that support the business, like rent, utilities, office supplies, and administrative salaries.

Unlike direct costs, indirect costs tend to be relatively stable and easier to control over time, making them more predictable in a business budget. This stability helps companies plan and allocate resources effectively.

An income statement lists indirect costs under the “Operating Expenses” section, representing the general costs of keeping the business running smoothly.

Examples of Indirect Costs

Examples of indirect costs include:

- Utilities: These are electricity, water, and gas expenses to keep the business operational.

- Consulting: This is comprised of fees paid to consultants who provide general business support.

- Legal and Financial Fees: These are costs for legal advice, accounting, or financial planning services.

- Administrative Expenses: These are general office expenses (e.g., supplies and support-staff salaries).

- Maintenance Expenses: These are costs for repairing and maintaining equipment or facilities.

- Phone and Internet: This is comprised of charges for communication and connectivity essentials for business operations.

- Rent: This is the cost of leasing office or warehouse space.

- Insurance: This is comprised of premiums for protecting the business against risks.

These essential expenses support overall business activities rather than any single product or project.

How to Allocate Indirect Costs

Allocating indirect costs accurately is essential for determining the true cost of products or projects and effective financial management.

Here are some common methods for allocating indirect costs:

- Direct Labor Method: This method allocates indirect costs based on the direct labor hours worked on a project or for a product. It assumes that the more labor-intensive a project is, the more indirect costs it incurs. To use this method, calculate the total indirect costs and divide them by the total direct labor hours to determine an overhead rate, which can be applied to each project based on the labor hours used.

- Direct Material Method: This method allocates indirect costs based on the direct materials used in production. It is suitable for businesses where material consumption is a significant driver of indirect costs. Like the labor method, total indirect costs are divided by the total direct material costs to establish a rate, which is then applied based on the direct materials used for each product or project.

- Sales Method: Under this method, indirect costs are allocated based on the proportion of sales revenue generated by each product or project. This approach is often used in sales-driven industries. To allocate costs, total indirect costs are divided by total sales revenue to determine a rate, which is then applied to each product based on its sales revenue.

- Activity-Based Costing (ABC): This more sophisticated method allocates indirect costs based on specific activities that drive those costs. It identifies all activities involved in production and assigns costs to each activity based on its use of resources. This allows for a more precise allocation, which reflects each product or project’s actual consumption of indirect costs.

- Percentage of Total Costs: In this simple method, indirect costs are allocated based on a fixed percentage of the total direct costs. This less-precise approach can be useful for quick estimates when detailed data is unavailable.

Direct Cost Vs Indirect Cost

The key differences between direct and indirect costs are:

- Connection to Product or Project: Direct costs (e.g., raw materials and labor) are directly tied to a specific product, project, or service. Indirect costs (e.g., utilities and administrative salaries) support the business as a whole rather than any single product or project.

- Cost Variability: Direct costs vary significantly with production levels and market conditions. Indirect costs are relatively stable over time, which makes them easier to predict and control.

- Income Statement Placement: Direct costs appear under the “Cost of Goods Sold” (COGS) section. Indirect costs are recorded in the “Operating Expenses” section.

The following table shows further differences between direct and indirect costs:

| Direct Costs | Indirect Costs |

| Direct costs affect the product or service price and are thus calculated per project or product. | Indirect costs affect the whole business and are thus calculated monthly or annually. |

| The product quantity affects the final product costs. | Changes in product quantity do not significantly affect the indirect cost. |

| They are highly variable due to market factors. | They are relatively stable. |

| They include raw materials, manufacturing, direct labor, and direct fuel costs. | They include rent, leases, utilities, insurance, legal fees, financial fees, office expenses, maintenance, and telecommunications. |

| They are included in the “Costs of Goods Sold” section on the income statement. | They are included in the “Operational Expenses” section on the income statement. |

Fuel, electricity, and administrative costs can be classified as “direct” or “indirect,” depending on the organization and specific project needs. For example, if fuel is used directly in production, it is a direct cost. Similarly, administrative costs might be considered direct if they directly support the production process.

Fixed Vs Variable Costs

Fixed costs and variable costs are two fundamental categories of business expenses that differ in their behavior relative to production levels.

Fixed costs are expenses that remain consistent—regardless of the level of production or sales. They do not change with the volume of goods or services produced (e.g., rent, permanent staff salaries, insurance, and equipment depreciation). These costs provide stability in budgeting but can burden a business during periods of low sales volume.

Variable costs fluctuate directly with production levels. They increase as production rises and decrease when production falls. Examples of variable costs include raw materials, direct labor, and utilities based on usage. This flexibility allows businesses to adjust their expenses based on operational demands.

| Direct Costs | Indirect Costs | ||

| Direct labor | Highly variable | Rent | Fixed |

| Raw materials | Highly variable | Lease | Fixed |

| Production supplies | Highly variable | Utilities | Fixed |

| Fuel costs | Variable, due to different fuel taxes per jurisdiction | Administrative costs | Variable |

Understanding the difference between fixed and variable costs is crucial for effective financial management, pricing strategies, and overall business planning. It can help you forecast profitability and manage cash flow.

Why Should You Know the Difference Between Direct and Indirect Costs?

Understanding the difference between direct and indirect costs is important for several reasons:

- Accurate Budgeting and Cost Control: Knowing the direct and indirect costs can help you set accurate budgets, control expenses, and avoid overspending. This will enable better financial planning and resource allocation.

- Pricing and Profitability: Direct costs directly impact the cost of producing a product or delivering a service. Businesses can set competitive pricing by managing these costs carefully while ensuring profitability.

- Tax and Financial Reporting: Different costs are treated separately on financial statements. Direct costs go under the Cost of Goods Sold (COGS), which affects gross profit, while indirect costs fall under Operating Expenses, which impacts operating profit. Correctly categorizing these costs will ensure compliance with financial reporting and tax regulations.

- Project Management: Distinguishing between direct and indirect costs is essential for controlling the budget, managing resources efficiently, and accurately calculating the total project cost.

- Strategic Decision-Making: Knowing how costs affect your business can help leaders make informed decisions. For instance, if indirect costs are too high, management may look for ways to improve efficiency across the business.

Understanding direct and indirect costs helps maintain financial health, ensure compliance, and support better business decisions.

How to Manage Direct and Indirect Costs

Managing direct and indirect costs effectively is crucial for maintaining profitability and ensuring operational efficiency.

Here are some tips for managing and reducing these costs:

- Negotiate with Suppliers: Building strong relationships can improve pricing and terms. Review contracts regularly and negotiate for discounts, bulk purchase deals, or favorable payment terms to lower direct costs.

- Improve Production Efficiency: Streamlining production processes can help you reduce direct costs. Implement lean manufacturing techniques, invest in employee training, or use technology to optimize workflows and minimize waste.

- Evaluate and Reduce Indirect Costs: Regularly assess indirect expenses (e.g., utilities, office supplies, and administrative salaries). Implement energy-saving measures, cut unnecessary subscriptions, or consolidate services to reduce these costs.

- Outsource Non-Essential Tasks: Consider outsourcing tasks that are not core to your business (e.g., accounting, customer service, or IT support). This can reduce overhead costs while allowing your team to focus on strategic activities that drive growth.

- Implement Budgeting and Monitoring Tools: Use budgeting software to track direct and indirect costs effectively. Regular monitoring can help you identify trends and areas for potential savings, thus allowing for timely adjustments.

- Encourage Employee Involvement: Foster a cost-conscious culture by involving employees in cost-management efforts. Encourage them to identify inefficiencies and suggest ways to save on direct and indirect costs.

By actively managing direct and indirect costs, businesses can enhance their profitability, streamline operations, and position themselves for long-term success.

Summary

Direct costs are closely linked to products or projects, directly impacting product pricing or project costs, while indirect costs support overall business operations without being tied to any single output. Understanding these two types of costs is essential for optimizing your business model, setting competitive prices, and distinguishing tax-deductible expenses.

Regularly reviewing both cost categories allows organizations to identify and control unnecessary spending, helping improve operational efficiency. By managing direct and indirect costs effectively, businesses can achieve greater financial clarity, enhance profitability, and make more informed strategic decisions.

Further Reading:

- Cost Estimation Tools in Project Management

- Project Cost Estimation: Examples and Techniques

- Cost of Quality: Cost of Conformance and Cost of Nonconformance

- Cost Benefit Analysis

References:

I am Mohammad Fahad Usmani, B.E. PMP, PMI-RMP. I have been blogging on project management topics since 2011. To date, thousands of professionals have passed the PMP exam using my resources.

I really enjoyed this article, very well written and easily digestable. thanks Fahad!